JPMorgan just filed for a Bitcoin product that Wall Street’s never seen before. It promises double-digit returns tied to the 2026-2028 halving cycle. But there’s a catch that could cost you everything.

This isn’t another spot ETF. It’s a structured derivative that treats Bitcoin like a high-stakes options contract. And it signals a major shift in how institutions plan to trade crypto through the next halving cycle.

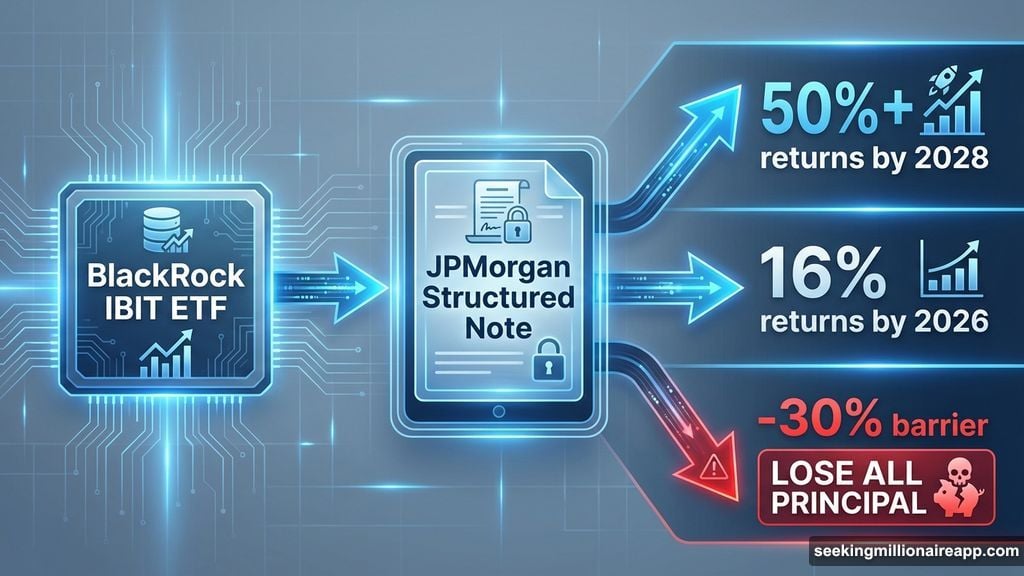

The Product That Pays 50% or Nothing

JPMorgan’s new structured note links directly to BlackRock’s IBIT Bitcoin ETF. The bank offers fixed returns if IBIT hits preset price targets. But if the ETF drops more than 30%, investors lose their entire principal.

Here’s the exact payout structure. If IBIT reaches JPMorgan’s target by the end of 2026, investors get 16% fixed returns. Hit that target by 2028 instead, and returns jump above 50%.

So what’s the risk? The note includes a 30% downside barrier. If IBIT falls beyond that threshold at any point before maturity, investors lose everything they put in. Not just gains. The entire principal investment.

JPMorgan states this clearly in their filing: “The notes do not guarantee any return of principal.” Once that 30% barrier breaks, losses match the ETF’s decline exactly.

This Is a Derivative, Not an Investment

The structure works nothing like owning Bitcoin or even holding IBIT shares. Instead, it functions as a contract whose payout depends on IBIT’s performance.

Think of it like this. You don’t own Bitcoin. You don’t own the ETF. You own a contract that says:

- IBIT hits target by 2026 → You get 16%

- IBIT hits target by 2028 → You get 50%+

- IBIT drops 30% → You lose your principal

That’s textbook derivatives trading. Plus, the note includes features borrowed straight from traditional equity derivatives:

- Auto-call triggers in 2026

- 30% downside barrier protection

- 1.5x leveraged upside with no cap

The leveraged upside is particularly revealing. That 1.5x amplification is identical to the payoff structure in long options positions. And losing 100% when IBIT breaks the barrier mirrors what happens when an option expires worthless.

“The spot ETF narrative is done, Wall Street’s institutions are starting to offer derivatives to everyone,” analyst AB Kuai Dong wrote on X.

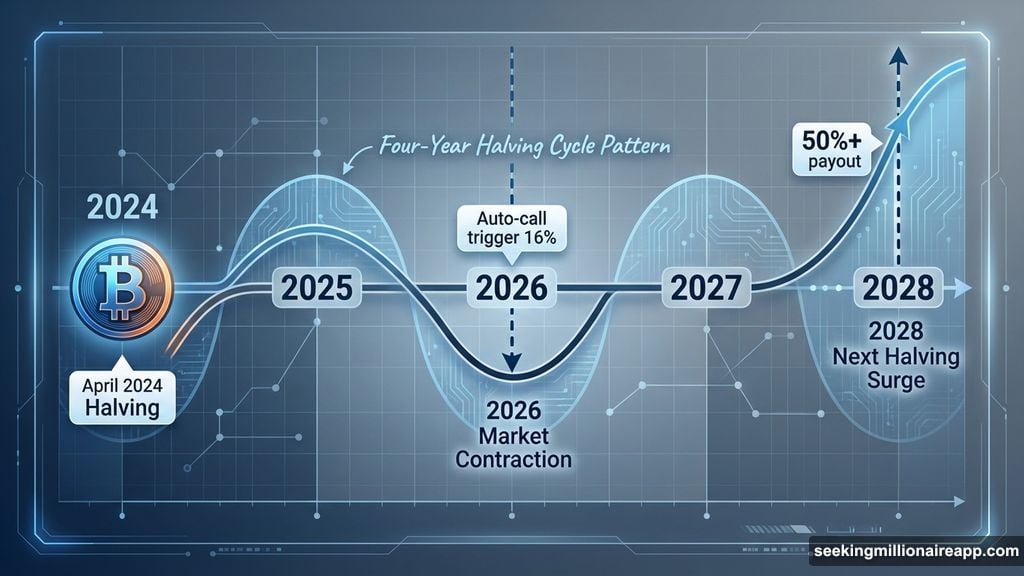

Why 2026 and 2028 Matter for Bitcoin

The timing isn’t random. JPMorgan engineered this product around Bitcoin’s four-year halving cycle, which has historically driven massive price movements.

The most recent halving happened in April 2024. That places the next expected market contraction around 2026, followed by a renewed surge into 2028—the next halving year.

Bitcoin tends to enter deep drawdowns roughly two years after each halving event. Then it rallies hard heading into the next halving. This pattern has repeated consistently across previous cycles.

JPMorgan’s note design maps directly onto this timeline:

2026 scenario: If IBIT hits the bank’s early target, the note auto-calls and pays 16% fixed returns. The contract ends.

2026-2028 scenario: If IBIT stays below target, the note remains active. Investors get 1.5x leveraged upside with no cap if Bitcoin rallies into 2028.

2028 outcome: Investors recover principal only if IBIT avoids that 30% decline through the entire period.

The structure essentially bets on Bitcoin following its historical halving pattern. Strong performance triggers early payout. Modest performance extends the contract with leveraged upside. Poor performance wipes the investment.

Wall Street Just Shifted From ETFs to Engineered Derivatives

This product signals that institutions are moving beyond simple spot ETF exposure. They’re now building complex derivatives engineered for yield, leverage, and asymmetric risk.

These tools mirror products traditional banks have used for decades in equities, commodities, and foreign exchange. Now they’re porting the same mechanics into digital assets.

For institutional investors, the appeal is clear. They can amplify returns without directly holding volatile Bitcoin. They get exposure to BTC price movements through a contract structured around familiar derivative principles.

But the risks are equally stark. Bitcoin has historically experienced drawdowns of 70% to 85% during bear markets. Hitting a 30% barrier isn’t uncommon even in mild corrections.

JPMorgan’s filing acknowledges this explicitly, warning that investors “could lose all” principal if the underlying ETF breaks the threshold.

What This Means for the Next Halving Cycle

The approval process will determine how soon this reaches institutional desks. But the design itself reveals three major trends:

First, more Wall Street-engineered products are coming. JPMorgan won’t be the last bank to build derivatives around Bitcoin ETFs. Expect similar structures from other major institutions.

Second, yield-seeking structures will dominate. Traditional investors want protected returns and leveraged upside. They’re less interested in simply holding volatile crypto assets.

Third, capital flows through derivatives rather than spot. Institutions prefer trading contracts based on Bitcoin’s performance over owning the actual asset or even spot ETFs.

As the market approaches the 2026 mid-cycle phase, demand for these protected-yield and leveraged-upside products will likely surge. JPMorgan’s move offers an early preview of how institutions plan to trade the next halving cycle.

The spot ETF era opened institutional access to Bitcoin. Now the derivatives era is engineering how that access gets structured, packaged, and sold.

The Real Risk Nobody’s Talking About

Here’s what bothers me about this product. It takes Bitcoin’s already high volatility and adds another layer of complexity that most investors won’t fully understand.

Bitcoin can absolutely drop 30% in a matter of weeks. It’s happened repeatedly throughout its history. So this barrier isn’t some theoretical risk—it’s a highly probable scenario.

Yet the product markets itself around upside potential. That 50% return grabs attention. The total loss risk gets buried in regulatory disclosures.

Moreover, this shifts how people think about Bitcoin exposure. Instead of understanding BTC as a volatile but potentially valuable asset, they see it as a structured bet with engineered payouts.

That’s not necessarily wrong. But it’s a very different approach than what Bitcoin was designed to enable. And it moves control firmly back to traditional financial institutions.

Still, this is where the market’s heading. Institutions want engineered products, not direct exposure. They want contracts, not custody. And they want Wall Street’s risk management tools applied to crypto assets.

JPMorgan’s filing shows exactly how that future looks. Whether that’s good for Bitcoin adoption or just good for bank profits remains an open question.