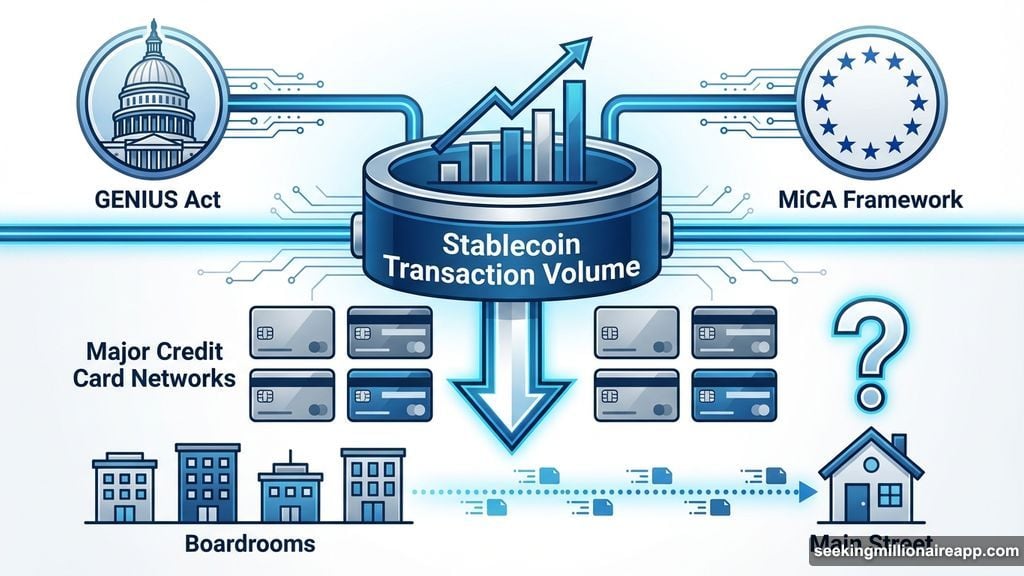

It’s February 2026, and something strange is happening. Crypto is woven into the fabric of global finance. Regulatory frameworks like the US GENIUS Act and the EU’s Markets in Crypto-Assets (MiCA) framework are fully operational. Stablecoin transaction volumes have surpassed major credit card networks in several payment corridors.

And yet, ask your neighbor if they use crypto daily, and they’ll probably look at you sideways.

That’s the paradox industry leaders are wrestling with right now. BeInCrypto sat down with a panel of builders and executives from Zoomex, BingX, BloFin, Kraken, Phemex, and Arcanum Foundation to understand why crypto feels ubiquitous in boardrooms but invisible on Main Street. Their collective answer? The technology is ready. The regulations exist. The final obstacle is something far harder to code away: culture.

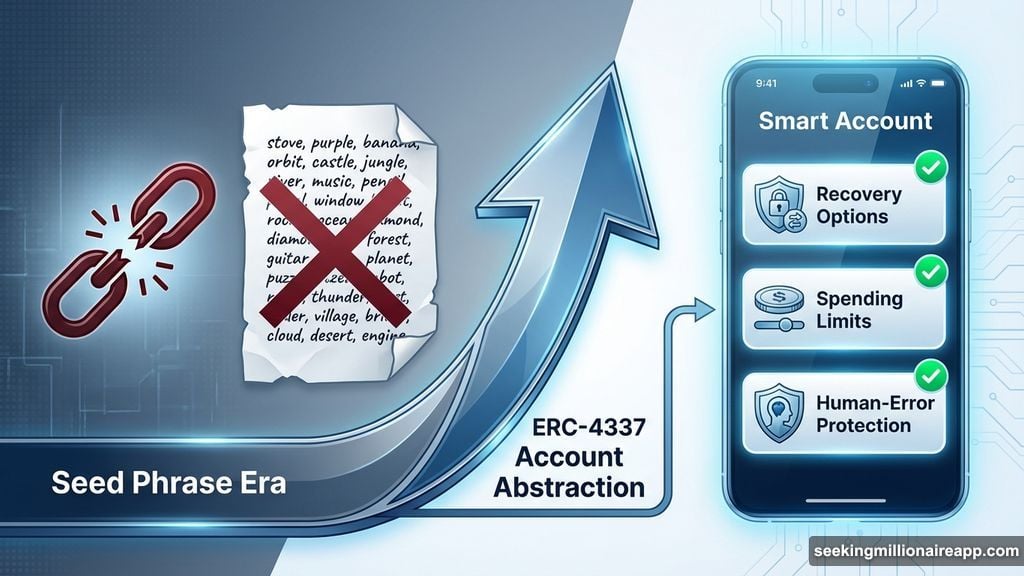

Smart Accounts Are Killing the Seed Phrase Era

For over a decade, one thing scared people away from crypto more than anything else. One mistake — a forgotten seed phrase, a typo in a wallet address — and your savings were gone forever. No customer service. No chargeback. Just silence.

That brutal reality shaped crypto’s reputation in ways that are still painful today.

Dorian Vincileoni, Head of Regional Growth at Kraken, doesn’t sugarcoat where things stand. “Can we honestly say a non-technical person is safe? Not entirely, and pretending otherwise would be dishonest. The user experience has improved dramatically, but self-custody still carries responsibility, and responsibility is not intuitive for everyone.”

But something fundamental has shifted. The binary choice between a centralized exchange and terrifying self-custody is disappearing. Instead, account abstraction standards like ERC-4337 are ushering in what the industry calls Smart Accounts — wallets with built-in recovery options, spending limits, and human-error protections.

Vincileoni explains the new mindset: “Better interfaces, account abstraction, and smarter safeguards are reducing the cost of human error. The real shift is not eliminating risk entirely, but giving users choices. Some will prefer full sovereignty, others will accept guardrails. Mass adoption will come from respecting both.”

Michael Ivanov, CEO of Arcanum Foundation, is building exactly that kind of safety net. His team developed Telegram Web Apps (TWA) with risk management layers specifically designed to protect users from costly mistakes. “We still have a long way to go for simplification of the entry journey,” Ivanov admits. “We have developed several TWAs with efficient risk management layers designed specifically to help users avoid losing their funds, even if they make several mistakes.”

The killer UX in 2026 isn’t a prettier interface. It’s a safety net that makes experimentation feel safe.

The Killer App Was Financial Infrastructure All Along

Remember when the crypto world hunted obsessively for the “killer app”? That one product that would onboard a billion users overnight? The NFT boom of 2021 promised it. Bitcoin ETFs dominated 2024. Neither delivered the mass moment everyone expected.

By 2026, most serious builders have quietly abandoned that hunt. Instead, they focused on something more pragmatic: making existing financial rails work ten times better.

Fernando Lillo Aranda, Marketing Director at Zoomex, calls this shift Convergence — the moment Web3 stops being a separate universe and starts bleeding into everyday financial life. “The real ‘killer app’ of 2026 is the convergence between Web3 financial infrastructure and everyday financial use cases,” Aranda explains.

So what does convergence actually look like in practice? It’s not on-chain governance dashboards or decentralized social networks. It’s crypto-linked debit cards that pay out real-time yield. It’s instant profit withdrawals for everyday spending. It’s high-yield savings alternatives that make traditional bank accounts look embarrassing.

“When Web3 stops feeling like a separate ecosystem and instead becomes a better financial layer for everyday life, adoption will follow naturally — not because of speculation, but because it simply works better,” Aranda adds.

Not every user enters through banking, though. Ivanov sees Web3-integrated MMO games as the on-ramp for younger, digital-native audiences. “For some, it’s crypto banking; for others, it’s an immersive economy where they actually own their digital progress.” His point is smart: mass adoption doesn’t require one door. It requires many doors, each built for a different person.

Stablecoin Transaction Volume Already Rivals Card Networks

Here’s a number that should stop you mid-scroll. In 2025, stablecoin transaction volume surpassed major credit card networks in several key payment corridors. That’s not a projection. It already happened.

Vivien Lin, Chief Product Officer at BingX, sees the transition clearly but warns against expecting a dramatic overnight shift. “We are moving in that direction, but it will be gradual rather than absolute. Stablecoins are increasingly being used for payments because they are fast, low-cost, and global — especially for cross-border commerce and online services.”

For many merchants, particularly those handling international payments, accepting stablecoins already beats dealing with traditional payment infrastructure. Settlement times drop from days to seconds. Fees shrink dramatically. Currency conversion headaches disappear.

But Lin adds an important reality check. “Fiat will not disappear from daily spending anytime soon.” The more likely outcome? Users simply won’t care about the distinction. Whether a digital payment runs on a CBDC, a bank-issued stablecoin, or a decentralized option like LUSD, the end user just wants it to work.

Griffin Ardern from BloFin offers a sobering macro perspective on why fiat won’t vanish globally anytime soon. “While many merchants are starting to accept stablecoins, they are currently treated more like ‘money market funds’ than fiat alternatives. Although the collateral risk of stablecoins is among the lowest in the crypto market, it is still significant compared to traditional tier-one assets.”

Geography matters enormously here. In countries with weak sovereign credit, people willingly accept stablecoin risk because the alternative is worse. In countries with stable currencies, adoption happens in targeted use cases rather than wholesale replacement. Merchants face similar logic — they’ll accept stablecoins, but in limited quantities to avoid unnecessary balance sheet risk.

Ivanov, however, already lives in the future. “I use crypto-linked cards almost everywhere in the world with no need to pay with fiat. However, we still need to push through government and regulatory issues in many countries to make this the standard, not the exception.”

The Trust Gap That Technology Can’t Fix

Here’s the uncomfortable truth. The technology works. The regulations provide a framework. The products are genuinely useful. So why isn’t adoption at 100%?

The answer isn’t in the code. It’s in people’s heads.

Federico Variola, CEO of Phemex, argues that the industry has reached a point where shipping more features won’t move the needle. “Mass adoption is closer than many think. Most younger users have already interacted with crypto in some form, and access has become much easier through centralized exchanges and intuitive wallets. The remaining challenge is perception.”

The collapses of 2022 and 2023 left scars that haven’t fully healed. FTX didn’t just lose people money. It confirmed every fear skeptics ever had about crypto being a rigged casino for insiders. “What’s needed now is a more constructive public narrative so skeptical users feel comfortable engaging,” Variola explains. “Adoption is less about building new tools and more about the market being in the right psychological conditions.”

Ivanov ties it all together with characteristic directness. “It is a complex web of reasons. Surely including regulation issues, a lingering lack of trust, and the fact that many Web3 apps still have a complicated usability profile for someone used to the simplicity of Instagram or Amazon.”

Building trust through transparency and education beats celebrity endorsements and price-action hype every single time. The industry is starting to understand that.

Crypto’s Biggest Moment Is the One You Don’t Notice

The experts at Zoomex, BingX, BloFin, Kraken, Phemex, and Arcanum have helped paint a picture of an industry that’s finally grown up. It stopped trying to burn down the banking system and started quietly upgrading the financial operating system underneath it.

Mass adoption doesn’t arrive as a revolution. It arrives as convenience.

It’s the debit card that earns you yield in real time. It’s the cross-border payment that settles in two seconds for almost nothing. It’s the game where your legendary sword has real-world liquidity. None of these moments announce themselves with a blockchain explorer or a whitepaper.

The tools are ready, as Variola notes. The world is simply deciding whether it’s ready to trust them. And based on what’s already happening quietly in payment corridors, gaming economies, and yield-bearing wallets around the world — that decision is already being made.

Look around. The answer is already here.