Binance isn’t staying quiet. The cryptocurrency exchange pushed back hard this week against a US Senate inquiry accusing it of helping Iran dodge international sanctions.

Co-CEO Richard Teng called the allegations “false and defamatory.” And the exchange didn’t stop there. It published a detailed blog post defending its compliance record while simultaneously threatening legal action against the Wall Street Journal over the original reporting that sparked the controversy.

The dispute lands at a genuinely tense moment for the entire crypto industry — one where congressional pressure and surging illicit activity are colliding in very public ways.

What Senator Blumenthal Actually Accused Binance Of

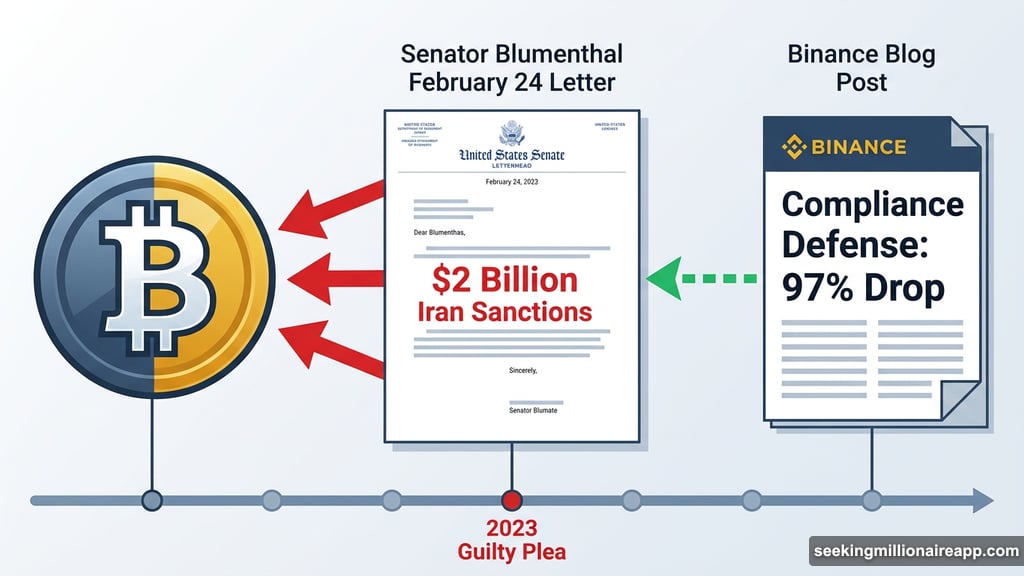

Senator Richard Blumenthal’s February 24 letter didn’t pull any punches. He accused Binance of enabling nearly $2 billion in transfers to sanctioned Iranian entities, and claimed the exchange had actively supported the activity rather than simply missing warning signs.

“Binance appears to have ignored clear warning signs, knowingly allowed illicit accounts to operate, and even provided hands-on support to entities engaged in money laundering,” Blumenthal wrote.

That’s a serious charge. And it got more damaging from there.

The senator revealed that Binance’s own compliance staff had flagged over 2,000 Iranian-linked accounts despite the platform’s stated ban on Iranian users. He also raised concerns about investigators who flagged the activity allegedly being fired afterward — a detail the exchange disputed.

Friday marked the subcommittee’s deadline for Binance to hand over the requested records. The exchange responded publicly through its blog post but stopped short of providing the specific documentation Blumenthal requested.

Binance’s Defense: 97% Drop and $752 Million Seized

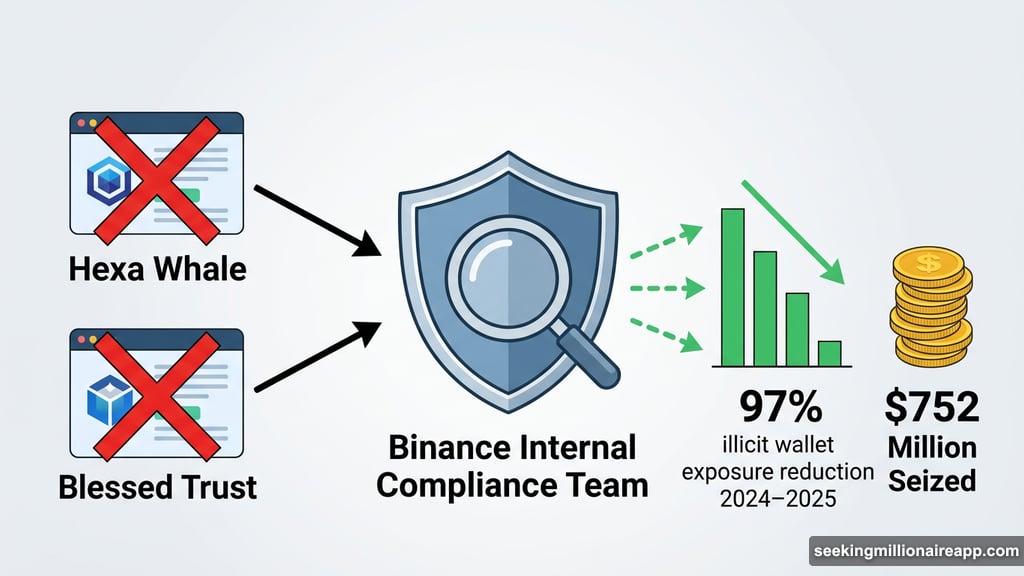

Binance came out swinging with numbers. The exchange cited a 97% drop in exposure to allegedly illicit wallets between early 2024 and mid-2025. Plus, it claimed to have helped law enforcement seize more than $752 million in illicit funds over the past three years.

On the fired investigators question, Binance said those employees were dismissed for breaching internal confidentiality policies — not for raising compliance concerns. The exchange framed their departure as a disciplinary matter unrelated to their compliance work.

Binance also confirmed it offboarded two exchange partners — Hexa Whale and Blessed Trust — after its own internal investigations identified them as potential intermediaries for Iranian money laundering. The exchange presented that move as evidence of proactive self-policing rather than regulatory failure.

The 2023 Guilty Plea Makes This Harder to Dismiss

Here’s where Binance’s defense gets complicated. The exchange isn’t starting from a clean slate on this topic.

In 2023, Binance pleaded guilty to federal charges for willfully transferring nearly a billion dollars to Iranian entities and terrorist organizations. Founder Changpeng Zhao received a four-month prison sentence as part of that resolution.

So when Blumenthal frames the current allegations as part of a “longer pattern of misconduct stretching back years,” that context matters. The exchange can point to improved compliance metrics, but the prior guilty plea gives the Senate inquiry real weight.

Blumenthal also raised the political dimension directly. He argued Binance had sought cover through its partnership with World Liberty Financial, a crypto venture tied to President Trump’s family. About 85% of World Liberty Financial’s stablecoins currently sit in Binance accounts. The SEC dropped its lawsuit against Binance last May, and Zhao received a presidential pardon shortly after.

Those connections don’t prove anything on their own. But they add a layer of complexity that senators are clearly paying attention to.

Crypto Crime Just Had Its Worst Year on Record

The timing of this showdown is particularly uncomfortable for Binance because the broader industry numbers are alarming.

According to a recent Chainalysis report, illicit addresses received at least $154 billion in crypto during 2025. That’s a 162% surge from the previous year. Most of that spike — a staggering 694% increase — came from funds flowing to sanctioned entities.

Chainalysis described the shift as a new era of large-scale nation-state activity linked to crypto crime. In other words, this isn’t random criminal behavior. It’s organized, it’s growing, and it’s directly relevant to exactly what the Senate is investigating.

Meanwhile, stablecoins accounted for 84% of all illicit transaction volume in 2025. That’s a dramatic shift from just 15% back in 2020. Tether has been specifically identified as a key vehicle in the Binance allegations, making the stablecoin angle central to the entire case.

Why This Goes Beyond Just Binance

The outcome of this Senate inquiry matters well beyond one exchange’s legal exposure.

Binance is the world’s largest crypto exchange by trading volume. How it handles congressional scrutiny — and how Congress responds — will likely influence how lawmakers approach broader crypto regulation. The industry is watching closely.

For Binance specifically, the stakes are straightforward. If its compliance record holds up under examination, the exchange can argue it has genuinely reformed since the 2023 guilty plea. If it doesn’t, the exchange faces potential new legal exposure at a time when it’s already navigating complex political relationships in Washington.

The $154 billion in illicit crypto flows recorded last year makes it nearly impossible for legislators to look the other way. And stablecoins sitting at the center of both that figure and the specific Binance allegations means this conversation isn’t going away quietly.

What happens next in this standoff will say a lot about whether crypto’s biggest players have truly cleaned up their operations — or just gotten better at talking about it.