If you’ve ever tried converting crypto to real spendable dollars, you know the pain. Bank accounts get frozen. Withdrawals take days. And sometimes your account just disappears without explanation.

EvoCash is betting it has the fix — and it’s building on solid regulatory ground to prove it.

The platform just launched USD-denominated digital accounts with real-time USDT-to-USD conversion, all backed by official Money Services Business (MSB) registration with FinCEN, the U.S. Financial Crimes Enforcement Network. That’s a big deal for anyone who’s been burned by the traditional banking system’s hostility toward crypto.

The Off-Ramp Problem Nobody Talks About Enough

Traditional banks weren’t built for crypto users. And they make that painfully obvious.

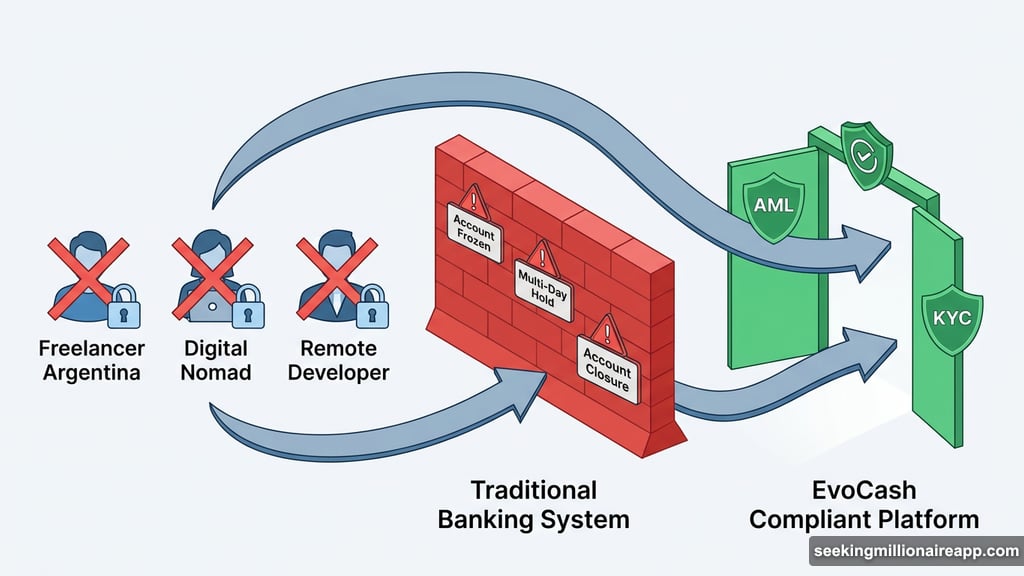

Freelancers, digital nomads, and international traders regularly run into account freezes after receiving crypto-related transfers. Multi-day holds on withdrawals are standard. Sudden account closures happen with zero warning. And if you’re earning crypto across borders? Most banks treat you like a suspect by default.

This isn’t just inconvenient. For someone like a developer in Argentina receiving USDT payments from U.S. clients, or a freelancer in Southeast Asia juggling multiple exchange accounts, these banking barriers create real financial hardship. The technology promises instant, borderless money. The banking system delivers the opposite.

“Banks weren’t built for the crypto economy, and their legacy systems treat digital asset users — especially international freelancers and remote workers — as high-risk by default,” the EvoCash team explained. Their solution: build a compliant alternative from scratch, purpose-built for exactly these users.

How EvoCash’s Compliance Structure Changes Things

EvoCash operates as a registered MSB under the Bank Secrecy Act. This matters because MSB registration lets the platform legally handle money transmission and currency exchange — including that critical stablecoin-to-USD conversion step that trips up so many crypto holders.

Rather than acting as a traditional bank, EvoCash partners with licensed financial institutions using For Benefit Of (FBO) account structures. That means client funds sit at the partner bank, kept completely separate from EvoCash’s own money. So your dollars are actually held by a regulated bank — just accessed through a much more crypto-friendly interface.

Plus, EvoCash includes full AML and KYC procedures aligned with FinCEN requirements. But unlike a traditional bank, it’s built around crypto users from day one. Legitimate transactions move smoothly instead of triggering endless red flags.

Real People, Real Problems This Solves

The platform’s approach clicks into focus when you look at specific use cases.

Consider a trader in Singapore converting $50,000 in USDT profits weekly for international business. With a traditional bank, that process meant submitting documentation, waiting three to five business days, and facing frequent account reviews. With EvoCash’s fiat off-ramp, that conversion happens in real time. Funds are immediately accessible.

Or take a freelance developer in Argentina receiving USDT from U.S. clients who needs those funds for everyday expenses. Previously, she needed multiple platforms — an exchange for conversion, a slow bank transfer, and constant worry about freezes. EvoCash’s digital dollar accounts for freelancers collapse that entire process into one step.

Then there’s the full-time digital nomad bouncing between Thailand, Mexico, and Portugal. Opening local bank accounts in each country is nearly impossible. International transfers carry heavy fees. EvoCash’s global onboarding gives users a Web3-compliant USD account that works from anywhere, no local banking relationships required.

What the Platform Actually Offers

EvoCash describes itself as a complete Web3 financial ecosystem rather than just a crypto-to-fiat bridge. The current feature set includes real-time stablecoin-to-USD conversion, bidirectional fiat on-ramp and off-ramp functionality, trading and exchange services across multiple crypto assets, multichain support across major blockchain networks, and cross-border USD payments accessible globally.

The platform is also pursuing a Visa card linked to stablecoins. Once approved by issuing partners, users would spend crypto-backed USD balances directly at merchants worldwide. That would close the loop entirely — earning, converting, and spending all within one compliant ecosystem.

Users also keep full connection to their Web3 wallets while accessing their digital dollar accounts. So you’re not choosing between DeFi access and compliant fiat functionality. You get both.

Why This Matters Right Now

The crypto off-ramp problem has existed for years. And it’s gotten worse as crypto adoption has grown faster than banking infrastructure has adapted.

International freelancers earning in USDT now make up a significant and growing slice of the global workforce. Cross-border businesses increasingly settle transactions in stablecoins. But the conversion layer — turning those digital dollars into spendable fiat — remains broken for millions of people outside the traditional banking mainstream.

EvoCash is targeting that exact gap. The MSB registration gives it a legal foundation that most crypto-adjacent fintech startups skip. The FBO account structure protects user funds. And the focus on global onboarding addresses users that traditional financial infrastructure has largely written off.

Whether it delivers on those promises at scale is something time will show. But the structure is smarter than most solutions we’ve seen try to crack this problem. For freelancers and digital nomads tired of fighting their own bank accounts, it’s worth watching closely.