The stock market had a rough Tuesday. And honestly, it was hard to be surprised once the numbers started rolling in.

Three separate forces hit investors at almost the same time. Hot wholesale inflation data arrived before the market even opened. Then the Federal Reserve confirmed it plans to keep rates higher for longer. And oil prices surged past $105 a barrel on news of Israeli strikes on Iranian energy facilities. Put all three together, and the selloff practically wrote itself.

Here’s what actually moved markets today and what investors are watching closely going into the rest of the week.

Hot PPI Data Crushed Rate Cut Hopes

The day started badly before the Fed even spoke. February’s Producer Price Index (PPI), which tracks wholesale prices before they hit consumers, came in more than double what economists expected.

Headline PPI landed at 3.4% year-over-year. That’s the highest reading since February 2025. Core PPI, which strips out food and energy, hit 3.9%. Nearly 30% of the entire increase traced back to diesel fuel prices, which surged a staggering 13.9%.

Traders who were quietly hoping for a rate cut by mid-year abandoned that idea fast. Markets quickly pushed expectations for any cut out to December at the earliest.

So by the time the Fed actually spoke, the market was already bracing for bad news.

The Fed Confirmed What Nobody Wanted to Hear

The Federal Open Market Committee (FOMC) held interest rates steady for the second straight meeting. That part wasn’t a shock. But the updated projections stung.

The Fed slashed its 2026 rate cut forecast to just one cut, down from three cuts projected earlier this year. The vote was 11-1, with Governor Miran casting the lone dissent. The Fed also revised its 2026 PCE inflation forecast higher to 2.7% and described the economic impact of Middle East tensions as “uncertain.”

Higher-for-longer just became official policy, at least for now.

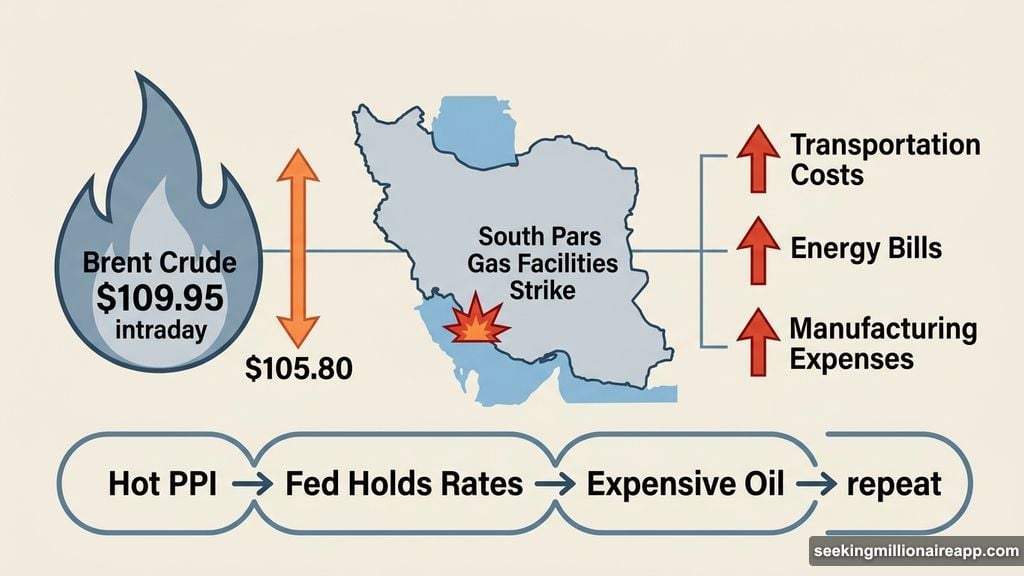

Brent Crude Above $105 Keeps Inflation Sticky

Oil didn’t help matters either. Brent crude hit $109.95 intraday before settling at $105.80, up 2.3% on the day. Israeli strikes on Iran’s South Pars gas facilities drove the spike.

At these price levels, crude oil feeds directly back into inflation. It raises transportation costs, energy bills, and manufacturing expenses. For the Fed, it makes cutting rates even harder to justify.

So the three forces fed each other in a loop. Hot PPI showed inflation isn’t cooling. The Fed confirmed it won’t cut rates. Expensive oil means inflation stays stubborn. Repeat.

Where the Major Indexes Finished

All three major US indexes closed lower at the time of writing:

- S&P 500: -0.60%

- Dow Jones: -0.87%

- Nasdaq: -0.56%

Small-cap stocks took the hardest hit overall. Higher rates hurt speculative and growth-dependent names first, and small caps carry the most of that exposure.

About 68% of stocks declined on the day. New lows crushed new highs at a ratio of 78.6% to 21.4%. On stock heatmaps, red dominated the screen almost completely. Microsoft fell 1.35%, Apple dropped 1.20%, and Amazon slid 1.90%.

The one bright spot on the map? Energy stocks. Refiners Marathon Petroleum and Valero each surged 2-4% as crude prices rose.

Technically, the S&P 500 Looks Fragile

Beyond today’s numbers, the chart for the S&P 500 deserves attention. The index has corrected nearly 5% since late February and is currently consolidating inside what technical analysts call a bear flag.

A bear flag forms when prices drift sideways after a sharp decline, often before breaking lower. Key levels to watch right now:

- Support zones: 6,650 and 6,620

- Bear flag target if it breaks: around 6,340, based on the prior 4.76% decline

- Recovery signal: needs to reclaim 6,740 and hold above 6,790

The bear flag hasn’t broken lower yet. But it’s pressing in that direction.

The Two Sectors That Stayed Green

Most sectors bled out today. But two held their ground for clear, logical reasons.

Energy gained 0.35% as Brent crude climbed above $105. Higher oil prices directly boost revenue for producers and widen profit margins for refiners. Phillips 66, Marathon Petroleum, and Valero each rose 5-9%.

Industrials squeezed out a 0.06% gain, largely thanks to defense contractors. RTX added 1.39% and GE Vernova climbed 3.55%. Ongoing Middle East military operations sustain government defense spending regardless of what’s happening in the broader economy. Wars don’t pause for rate hikes.

Basic Materials and Healthcare Led the Losses

On the other end of the spectrum, several sectors took meaningful hits.

Basic Materials fell 2.43%. Gold dropped about 5% on the week to $4,886, while silver tumbled roughly 10% to $77. A stronger dollar made those moves worse. When the Fed signals higher rates, the dollar strengthens, which makes gold and silver more expensive for international buyers. Plus, higher rates raise the opportunity cost of holding non-yielding assets like precious metals. Investors sell.

Consumer Defensive dropped 1.99%. Walmart fell 2% and Procter & Gamble slid 2.42%. Sticky inflation squeezes household budgets at the same time that elevated borrowing costs slow consumer spending. Defensive consumer stocks aren’t immune to that pressure.

Healthcare shed 1.32%. AbbVie led losses, falling 4.67% after the FDA approved Icotyde, the first oral pill for plaque psoriasis. That approval directly competes with AbbVie’s blockbuster drug Skyrizi. Eli Lilly also dropped 1.67%. Higher discount rates compress the future value of drug revenues, hitting healthcare valuations broadly.

What Happened With Nvidia and AbbVie

Two individual stocks stood out for opposite reasons today.

Nvidia (NVDA) managed to hold steady, gaining 0.40% to close around $184 despite the broader selloff. The company’s GTC conference in San Jose kept AI spending front and center. Analyst firm Rosenblatt raised its price target to $325 from $300 and reiterated a buy rating. AI investment remains the one story the market hasn’t given up on.

AbbVie (ABBV) wasn’t so lucky. The FDA’s approval of Icotyde, Johnson & Johnson’s competing psoriasis treatment, hit AbbVie shares hard. Skyrizi generates billions in annual revenue for AbbVie, so a competing oral option is a genuine long-term threat. A 4.67% drop in a single session reflects how seriously investors took the news.

What to Watch From Here

The FOMC dot plot has spoken clearly. One rate cut in 2026, one in 2027. Fed Chair Powell’s post-meeting press conference language around oil prices and their pass-through into consumer inflation will give markets one final read for today.

But the direction feels set. The stagflation rotation that’s been building for weeks stays firmly in play. Energy and defense remain the consistent outperformers. Oil above $100 keeps feeding inflation expectations. Gold and silver are correcting as the dollar strengthens. And the bear flag on the S&P 500 hasn’t broken yet, but it’s pressing harder.

If crude stays elevated, the playbook favors energy and defensives over growth and tech. The market just confirmed that today with about as much clarity as you’re going to get from a single session.