The debate has been going on for years. Private blockchains versus public ones. Controlled versus open. Compliance versus composability. Institutions weighed both sides carefully before committing capital.

Well, the capital has spoken. And the numbers are hard to argue with.

As of March 2026, nearly $16 billion in distributed real-world asset (RWA) value sits on Ethereum alone. That’s not a forecast or a projection. That’s live capital, deployed on a permissionless public chain, right now.

Two Types of On-Chain Value Nobody Explains Clearly

Before diving into the data, it helps to understand what “distributed” versus “represented” actually means. These two terms sit at the heart of the permissioned vs. permissionless blockchain debate, and most coverage glosses right over them.

Distributed assets use the blockchain as a genuine distribution layer. Investors hold assets in their own wallets. They can transfer them, use them as collateral in lending protocols, or trade them on decentralized exchanges (DEXs). The asset is composable and liquid.

Represented assets use the blockchain differently. It’s more like a digital filing cabinet. The blockchain records transactions for transparency and reconciliation purposes, but investors can’t actually move or use those assets on-chain. It’s a bookkeeping tool, not a financial infrastructure layer.

That distinction matters enormously when reading the data.

Ethereum Leads Distributed RWA Value. By a Lot.

According to rwa.xyz data from March 19, 2026, Ethereum leads all blockchains in distributed RWA value at nearly $16 billion. BNB Chain follows at $3.2 billion. Solana sits at $1.8 billion.

Tokenized funds drove most of that growth. Think treasury bills (T-bills), bonds, and money market funds (MMFs). These products now live on public blockchain infrastructure, accessible to global liquidity pools and DeFi protocols.

On the represented side, Canton dominates at $352 billion. That number sounds massive compared to Ethereum’s $16 billion. But the comparison isn’t apples to apples. Canton’s figure represents institutional record-keeping on a closed permissioned network. It’s not investor-held capital. It’s not deployable liquidity. It’s a ledger.

Private Blockchains Face a Structural Problem

Sandy Kaul, Head of Innovation at Franklin Templeton, told BeInCrypto something that cuts straight to the core of this debate.

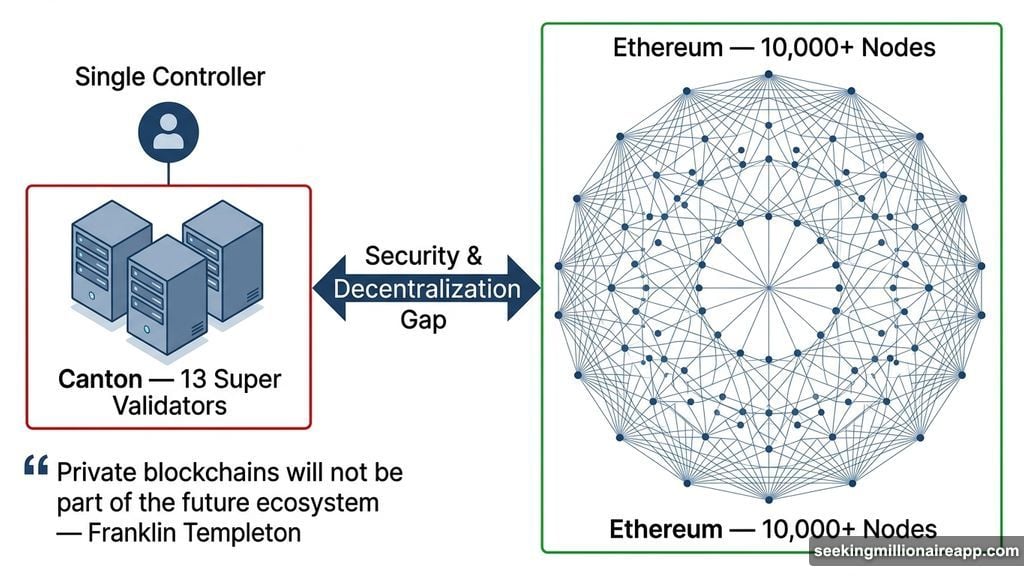

“I believe very strongly that private blockchains will not be part of the future ecosystem,” she said. “When you look at a private blockchain, it is typically built by a small team of 50 or 60 people. One entity runs it, and one entity is responsible for all transaction verification.”

The numbers back her up. Canton runs 13 Super Validators. Ethereum runs over 10,000 nodes. That’s not an incremental difference in security. That’s a completely different category of infrastructure.

Kaul went further, explaining the appeal of public chains. “Ethereum has over 4,000 developers and pays bug bounties to incentivize the discovery of security flaws. With over 10,000 different nodes verifying transactions, you need 51% consensus to validate data. The odds of a fraudulent transaction are statistically lower because the decentralization required to manipulate the network is so vast.”

Every Major Tokenized Fund on Ethereum Is Permissioned. That’s Actually Fine.

Here’s something that surprises people at first. The biggest tokenized funds on Ethereum all require wallet whitelisting and KYC (know your customer) verification. They’re permissioned products sitting on a permissionless base layer.

The current Ethereum RWA landscape includes some serious institutional names:

- BlackRock BUIDL: $785 million in active market cap

- WisdomTree Treasury Money Market: $619 million

- BlackRock USD Institutional (BUIDL-I): $481 million

- Plus significant holdings from Fidelity, Ondo, and Superstate

All of them require identity verification before access. Regulated securities demand that. There’s no way around compliance requirements.

But here’s why the permissionless base layer still wins. Institutions need global liquidity. They need 24/7 settlement. They need third-party protocols to build around their products without asking anyone’s permission first. A private, permissioned chain can’t offer all three simultaneously. A public chain can.

Matt Hougan, Chief Investment Officer at Bitwise Asset Management, articulated this well on the BeInCrypto Expert Council video panel. “My ultimate view is that permissionless, open architecture of blockchains will win, particularly as we unlock AML KYC, maybe using zero-knowledge proofs. The world wants to be in an open ecosystem. That’s the way tech has generally played out over time.”

He acknowledged institutions are still feeling their way forward. “You are going to see these more permissioned experiments because institutions are just sort of putting their toes into the water. And it takes comfort to get to the far end. My base case, though, is permissionless.”

Standard Chartered and R3 Corda Both Point the Same Direction

Geoff Kendrick, Global Head of Digital Asset Research at Standard Chartered, reinforced that view on the same panel. “I agree with Matt that in the long term, permissionless wins. And I think even more directly than that, I think Ethereum probably wins for the next little while on the back of TradFi getting involved.”

Even builders of private chain infrastructure are reading the same writing on the wall. R3 Corda holds over $10 billion in tokenized RWAs on permissioned networks used by major institutions including HSBC and Bank of America. Yet in 2025, R3 announced a partnership with Solana, seemingly to tap into public liquidity. A private chain company reaching for public rails is a telling signal about where the industry sees long-term value.

Aave Horizon Tests Whether RWA Collateral Works Inside DeFi

Capital flowing into permissioned tokens on open rails is one part of the story. The other part is whether that capital actually gets deployed inside decentralized finance (DeFi) protocols. Aave Horizon is the live experiment answering that question.

Horizon allows permissioned institutional borrowing using RWA collateral alongside permissionless stablecoin lending, all on Ethereum. The concept is straightforward and sensible. The early data tells a more complex story.

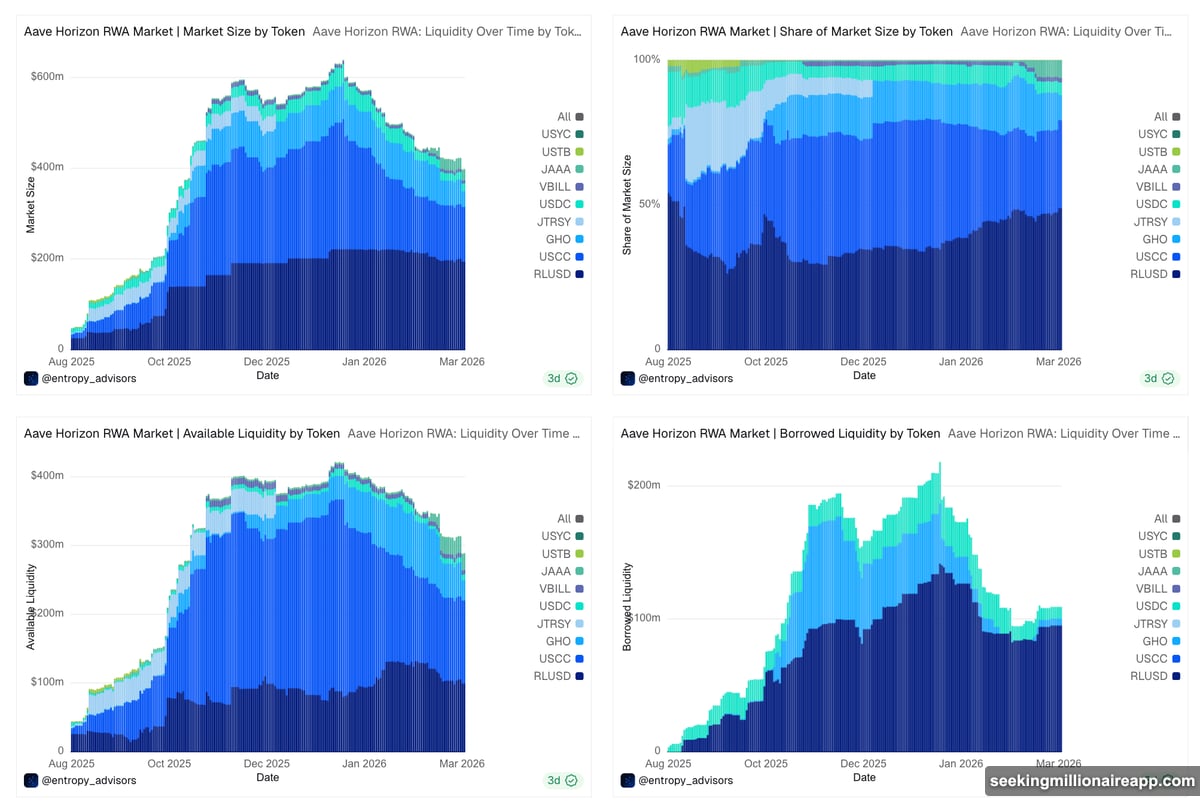

Aave’s permissionless protocol holds roughly $42 billion in total value locked (TVL) as of March 2026, according to DefiLlama. Horizon, the permissioned RWA arm of the same protocol, peaked near $600 million in market size in December 2025. By early 2026, it had declined toward the $350 to $400 million range. That puts Horizon at under 1% of Aave’s total TVL, despite being the product specifically designed for institutional participants.

Horizon’s Collateral Numbers Show Hybrid Adoption Is Still Early

Dune Analytics data from entropy_advisors and mrvega14 paints a granular picture of Horizon’s current state. Collateral inflows dropped from roughly $300 million in late 2025 to $141 million by February 2026.

Of that $141 million, Superstate Crypto Carry Fund (USCC) accounts for $123 million. That means a single product carries nearly 87% of all remaining collateral. Concentration at that level is a red flag for broader institutional adoption.

Janus Henderson’s treasury product (JTRSY) and US Yield Coin (USYC) both went to zero. Active wallet addresses peaked above 70 per day in October 2025 and now average between 20 and 30. Borrowed liquidity peaked around $200 million in January 2026 and has been falling since.

So Horizon isn’t failing exactly, but it’s not thriving either. The hybrid model is still finding its footing. The gap between institutional intent and actual on-chain activity remains significant.

Where the Capital Is Tells You Where This Ends

Step back and look at the full picture. You have nearly $16 billion in distributed RWA value on Ethereum. You have every major institutional tokenized fund choosing public blockchain infrastructure for distribution. You have leading voices from Franklin Templeton, Bitwise, and Standard Chartered all pointing toward permissionless as the long-term winner. And you have even private chain builders partnering with public networks to access liquidity they can’t generate internally.

Horizon’s early struggles don’t undermine the larger trend. They show that hybrid models take time to mature. Capital is already moving to public rails. The next chapter is whether that capital gets actively deployed inside DeFi protocols, or just sits there as collateral waiting for confidence to build.

The permissioned versus permissionless blockchain debate produced a clear winner in terms of where capital chooses to live. Every data point from March 2026 confirms it. The only real question left is how quickly the rest of institutional finance catches up to what the numbers already show.