The US stock market had a rough Friday. And honestly, it’s hard to blame anyone for selling.

The S&P 500 dropped 0.92%, marking its fifth straight weekly decline. Meanwhile, rate hike odds crossed 50% for the first time, bond yields hit new highs, and the Iran conflict showed zero signs of cooling down. Three separate problems all pointing to the same uncomfortable truth — oil above $100 is driving everything right now.

Rate Hike Probability Crosses 51% as Fed Cuts Disappear Until 2027

This is the number that spooked markets most on Friday.

The CME FedWatch Tool now shows no expected rate cuts until December 2027. More alarming, there’s a 51% probability of a rate hike by March 2027. That means rate hikes are now more likely than rate cuts — a dramatic reversal from earlier this year.

Why the shift? Surging oil prices keep feeding inflation expectations. The Fed simply can’t ease policy when energy costs are pushing prices higher across the economy. And when rates stay elevated or climb further, earnings multiples compress and risk assets become a lot less attractive to investors.

So the market isn’t just worried about the present. It’s worried about what the next 12 to 18 months look like if oil stays stubbornly above $100.

10-Year Treasury Yield Hits 4.48%, Squeezing Growth Stocks

Bond yields don’t move in isolation. When they climb, everything else feels the pain.

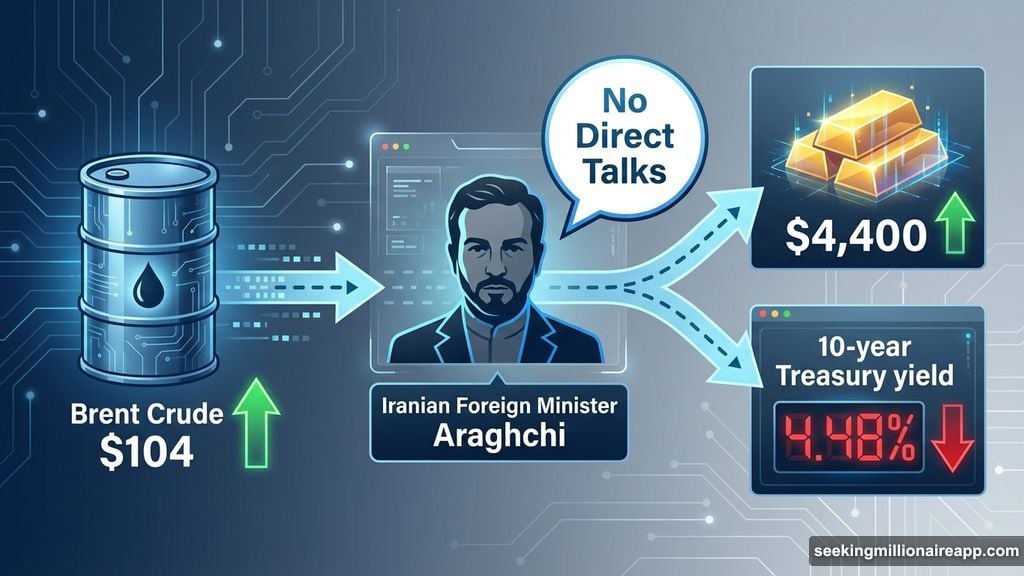

The 10-year Treasury yield jumped to 4.48%, its highest point since the Iran conflict began. That level puts the bond market in what analysts at The Kobeissi Letter are calling near “crisis” territory. Rising yields hit growth stocks particularly hard because they make future earnings worth less in today’s dollars.

The stronger US Dollar Index (DXY) adds another layer of pressure. Over 40% of S&P 500 revenue comes from overseas operations. When the dollar strengthens, foreign earnings translate back into fewer dollars at home. That quietly erodes profits for dozens of major companies across the index.

Meanwhile, investors looking for safety are piling into gold above $4,400 and silver. Hard assets are winning the flight-to-safety trade right now, pulling capital away from equities.

Iran Rejects Direct Talks, Brent Crude Holds Above $104

Oil isn’t budging. And that’s the core of every problem facing markets this week.

Iranian Foreign Minister Abbas Araghchi stated that exchanges through mediators don’t count as direct negotiations with the United States. That rejection kept Brent crude above $104 per barrel, maintaining the geopolitical risk premium that’s been baked into energy prices throughout the conflict.

Oil above $100 functions essentially as a tax. Businesses pay more for inputs. Consumers spend more at the pump. Discretionary spending shrinks. All of that flows through to corporate earnings, and markets price it in quickly.

How the Major Indexes Closed Friday

All three major US indexes finished in the red:

- S&P 500: Down 59.53 points, or 0.92%, at 6,417

- Dow Jones Industrial Average: Down 467.58 points, or 1.02%, at 45,492

- Nasdaq Composite: Down 279.90 points, or 1.31%, at 21,128

Market breadth told an equally grim story. A total of 3,746 stocks declined versus just 1,593 advancing. That’s not a rotation — that’s broad-based selling across almost everything.

Technically, the S&P 500 broke down from a bear flag pattern starting March 18, delivering a 3.8% correction so far. The measured move target sits at 6,347. If the index can’t reclaim 6,435, that target and an even lower level of 6,213 come into play next week.

Energy and Commodities Lead, Consumer Stocks Take the Worst Hit

Not every sector suffered equally on Friday. Energy actually had a good day.

The energy sector gained 1.51% as elevated oil prices directly boosted producer revenue. Exxon Mobil (XOM) rose 3.17% and Chevron (CVX) climbed 1.98%. Basic materials added 1.17% as investors rotated into commodities. Gold above $4,400 and strengthening silver prices made mining stocks an attractive inflation and geopolitical hedge. Utilities gained 1.08% as defensive positioning outweighed the typical rate sensitivity of the sector — nervous capital needs somewhere to park.

On the losing side, Consumer Cyclical stocks dropped 1.83%, the worst-performing sector of the day. Amazon (AMZN) fell 3.38% and Tesla (TSLA) dropped 1.83%. High oil prices drain consumer spending power, and that hits discretionary businesses fast.

Communication Services fell 1.41%, with Meta (META) dropping 3.65%. Ad-dependent companies are early casualties when slowdowns loom because advertising budgets get cut before almost anything else.

Financials declined 1.30% as the speed of the yield surge — combined with recession fears — raised credit risk concerns that outweighed any benefit from wider net interest margins. Technology lost 1.07% as the Nasdaq entered correction territory and high bond yields crushed growth stock valuations further.

Unity Surges, CrowdStrike and Cybersecurity Stocks Slide

A couple of individual stock stories stood out on Friday, for very different reasons.

Unity Software (U) surged roughly 10% after preliminary Q1 revenue came in at $505 million to $508 million, crushing prior guidance. The company also announced plans to sell its China division for over $1 billion, streamlining its focus around its AI-powered Vector advertising platform.

CrowdStrike (CRWD) told a different story. Shares fell about 7% after FY27 guidance landed below expectations, and AI-powered rivals intensified competitive pressure across cybersecurity. The pain spread sector-wide — Palo Alto Networks (PANW) dropped 7.2%, Cloudflare (NET) fell 3.75%, Zscaler (ZS) lost 7.6%, and Okta (OKTA) declined 6.7%. An Anthropic AI model leak reportedly showed strong cybersecurity capabilities, rattling confidence across the entire space.

Iran’s Counter-Proposal Could Define Monday’s Open

Iran’s response to President Trump’s 15-point peace plan is expected to arrive Friday via intermediaries, according to sources cited by Walter Bloomberg on X. That makes this weekend genuinely consequential for markets.

If Iran’s counter-proposal signals any real willingness to negotiate, oil prices could pull back meaningfully. That would give equities room to recover by Monday’s open. If the proposal amounts to another rejection, yields could push above 4.50% next week, and the S&P 500’s 6,347 technical target becomes a real destination rather than a distant possibility.

This weekend could end up being the most important 48-hour window for markets since the Iran conflict first began. Whether that’s cause for cautious optimism or preparation for more turbulence depends entirely on what arrives from Tehran.