Here’s a number worth sitting with: stablecoins handled $28 trillion in real economic activity in 2025. Not speculative trading. Not paper gains. Actual money moving through actual transactions.

And according to a new Chainalysis report, that figure could balloon to $1.5 quadrillion by 2035. That’s not a typo. That’s a quadrillion with a Q — a number so large it makes today’s global payments infrastructure look like a corner store.

Two massive forces are pushing this shift. And both of them are already in motion.

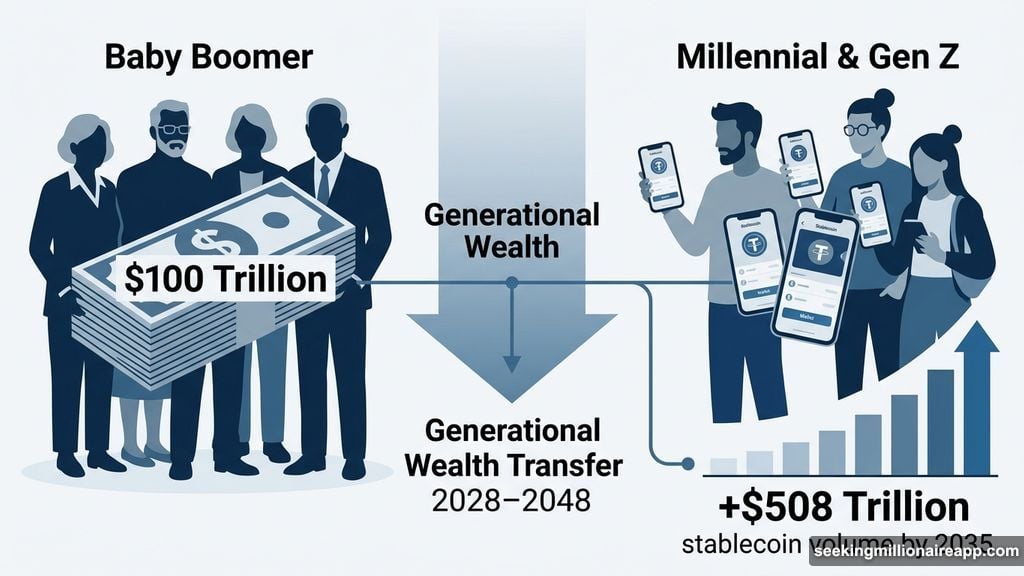

The Biggest Wealth Transfer in Human History

Starting around 2028, Millennials and Gen Z will become the majority of adults in North America and Europe. That demographic shift sounds straightforward. The financial implications, however, are enormous.

Merrill Lynch estimates that up to $100 trillion will pass from Baby Boomers to younger generations by 2048. That’s decades of accumulated wealth changing hands. And the people receiving it have a very different relationship with money than their parents did.

Nearly half of Millennials and Gen Z already own or have previously owned crypto, according to a 2025 Gemini survey. For them, moving money through crypto rails isn’t a bold experiment. It’s just how things work.

Chainalysis projects that behavioral shift alone could add $508 trillion to annual stablecoin volumes by 2035. To put that in perspective, that single number exceeds the entire current global cross-border payments market.

Merchant Adoption Changes Everything

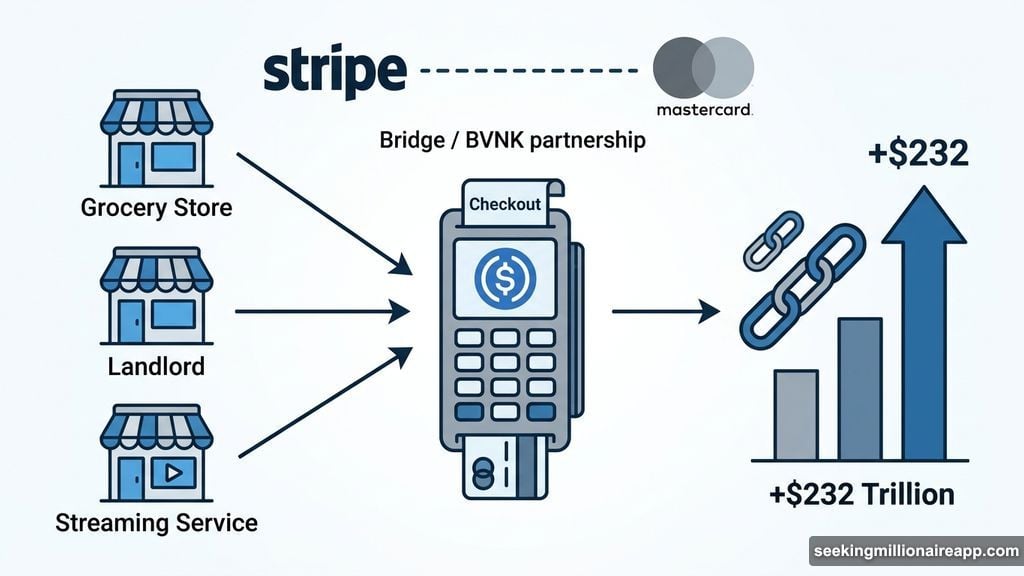

The second driver is quieter but equally powerful. When enough stores accept stablecoins, paying with crypto stops feeling like a deliberate tech-forward choice. It just becomes how you pay.

Major retailers and payment processors are already testing stablecoin integration at checkout. That might seem minor right now. But think about what happens when your grocery store, landlord, and streaming subscriptions all accept stablecoin payments. Every one of those routine transactions becomes on-chain activity.

At scale, that’s extraordinary. Chainalysis estimates that merchant adoption at the point of sale could add another $232 trillion to annual stablecoin volumes by 2035. Combined with the generational wealth transfer, the numbers start to feel almost incomprehensible.

Traditional Finance Is Already Positioning

Here’s the part that tells you how serious this is: the biggest names in traditional finance aren’t watching from the sidelines anymore.

Stripe bought Bridge. Mastercard partnered with BVNK. These aren’t exploratory partnerships or PR moves. These are institutions placing real bets on stablecoin rails becoming the backbone of future payments.

And the appeal makes practical sense. Stablecoins settle in seconds, operate around the clock, and cut out layers of intermediaries that have historically taken a slice of every transaction. For businesses processing millions of payments, those efficiencies add up fast.

Based on current trajectory, Chainalysis projects stablecoin transaction volumes could match the combined scale of Visa and Mastercard somewhere between 2031 and 2039. That’s not replacing those networks overnight. But it signals a world where stablecoins aren’t a niche alternative — they’re infrastructure.

What This Means for the Payments Industry

For the institutions that move slowly, the risk is stark. Those who wait may find themselves forced to settle transactions on someone else’s rails — paying fees to networks they could have built or joined years earlier.

For everyday people, the change will feel gradual and then suddenly obvious. Stablecoins won’t announce their takeover of payments. They’ll just quietly become the default option, one checkout screen at a time.

The $28 trillion already processed in 2025 isn’t a ceiling. It’s a starting point. And the combination of generational wealth transfer, merchant adoption, and institutional buy-in suggests the payments industry is entering a period of change it hasn’t seen since credit cards went mainstream. Whether you’re a business, a bank, or someone who just wants to send money quickly without paying a 5% wire fee, that shift is worth paying attention to.