The White House wanted a deal by the end of February. It didn’t happen.

Fresh reports from sources close to the negotiations confirm that the CLARITY Act’s stablecoin yield talks have stalled again. Banks and crypto firms remain far apart on a single flashpoint issue, and that disagreement is now threatening to derail the entire crypto market structure framework.

Stablecoin Yield Splits Banks and Crypto Firms

The core fight is surprisingly simple to understand. Should stablecoins be allowed to pay interest or rewards to holders?

Banks say no. Their argument is that yield-bearing stablecoins would function like unregulated bank deposits, giving crypto firms a competitive edge without the same regulatory burden traditional banks carry.

Crypto firms say that’s nonsense. Coinbase CEO Brian Armstrong has publicly argued that stablecoins can generate yield responsibly and that blocking those rewards would hurt innovation and ordinary users.

Neither side is budging. And until they do, nothing else moves.

Where the CLARITY Act Actually Stands

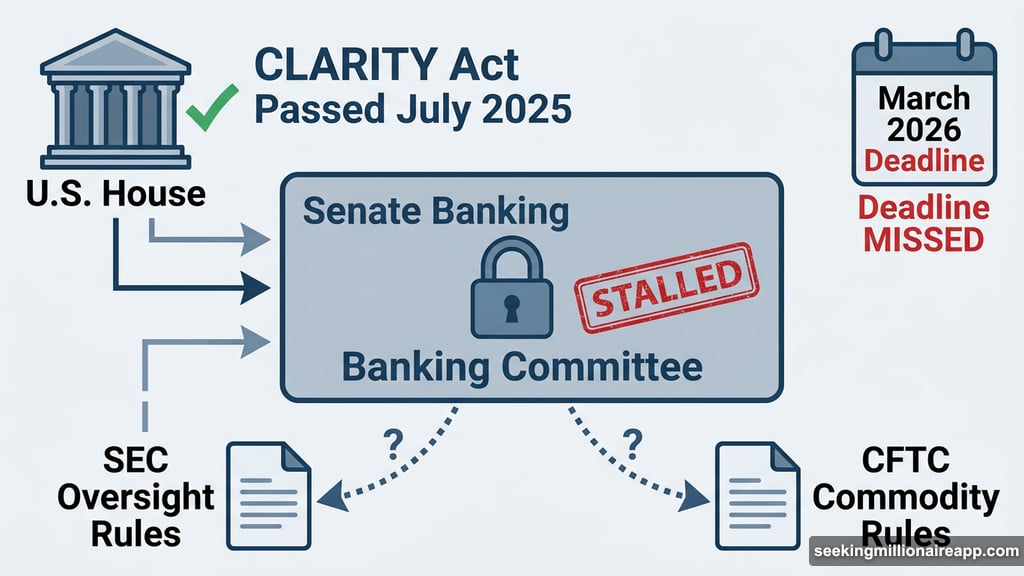

The House passed the CLARITY Act back in July 2025 with bipartisan support. At its core, the bill draws a clearer line between when digital assets fall under SEC oversight versus CFTC commodity rules. It also establishes registration requirements for exchanges, brokers, and custodians.

That part of the bill is largely agreed upon. But after passing the House, the legislation moved to the Senate Banking Committee and stalled almost immediately.

No markup has been completed. No floor vote is scheduled. The bill is sitting in committee while negotiators argue about stablecoin economics.

Then in early 2026, Senate negotiators introduced draft language restricting interest and yield payments on stablecoin holdings. That amendment shifted the entire debate and drew immediate opposition from major crypto players, including Coinbase, which publicly rejected the updated version.

Draft Language Exists, But Nothing Is Close to Final

According to journalist Eleanor Terrett, banking-side sources described the current state of talks bluntly. Draft language exists, but the two sides are “not close” to agreement.

Bank trade groups including the American Bankers Association and the Independent Community Bankers of America pushed back on claims the negotiations are collapsing entirely. They say discussions are ongoing and that input on draft text continues.

But that split narrative actually tells the story. Both sides are technically still talking. Neither side is ready to sign off on anything.

White House officials reportedly convened meetings between banks and crypto representatives in recent weeks, pushing for a yield deal before March. That deadline passed without a breakthrough.

Four Issues Still Need Resolution

The stalled talks involve four unresolved questions:

- Whether stablecoin rewards legally count as prohibited interest payments

- How sharply the bill should restrict exchange incentive programs

- Where exactly the boundary sits between SEC and CFTC authority over digital assets

- How broadly DeFi developers would be obligated to comply with new rules

None of these are minor technical details. Each one represents a fundamental disagreement about how crypto fits into existing financial regulation. Until yield language gets resolved, the broader market structure reforms cannot move forward.

SEC and CFTC Jurisdiction Still in Play

Beyond the stablecoin fight, the SEC-versus-CFTC boundary remains genuinely complicated. The original bill aimed to clarify which digital assets qualify as securities under SEC oversight and which qualify as commodities under the CFTC.

That clarity matters enormously for exchanges and developers who currently operate under significant legal uncertainty. Projects have faced enforcement actions without clear rules. Exchanges have struggled to know which regulator they answer to.

The CLARITY Act was supposed to fix that. But the stablecoin yield dispute has overshadowed the jurisdictional question and slowed the entire legislative process.

As analyst Austin Campbell noted publicly, if no deal is reached on the CLARITY Act language, the broader Genius Act language controls instead, which offers wider regulatory scope. That possibility gives banks less leverage than they might think, and it might ultimately push negotiators toward compromise.

What Happens Next

The next critical milestone is a Senate Banking Committee markup session. No date has been announced yet.

If negotiators manage to narrow their differences in March, a committee vote could follow later in the month. That would keep a path open for broader Senate consideration before the political calendar gets complicated.

But if talks drag through spring without resolution, the CLARITY Act risks sliding into election-year politics, where controversial legislation tends to die quietly. Both parties broadly support clearer crypto rules, but broad support doesn’t always translate into floor votes when political timing gets messy.

The bill is alive. It is not dead. But it is stuck, and the clock is ticking.

The real question at this point isn’t whether Congress wants crypto regulation. Most legislators agree that clearer rules would benefit markets, investors, and innovation. The question is whether banks and crypto firms can agree on who gets to control stablecoin economics, and whether either side is willing to compromise before this window closes.