The crypto world has a new fight on its hands. And this time, it’s not about price swings or exchange drama.

A freshly drafted bipartisan tax bill called the PARITY Act is drawing serious fire from Bitcoin advocates. They say the legislation creates an uneven playing field that punishes miners while quietly rewarding stakers. And the industry isn’t staying quiet about it.

What the PARITY Act Actually Proposes

The bill was circulated by US Representatives Max Miller and Steven Horsford. Its stated goal sounds reasonable enough: clean up how the Internal Revenue Code handles digital asset taxation in America.

But the details are where things get messy.

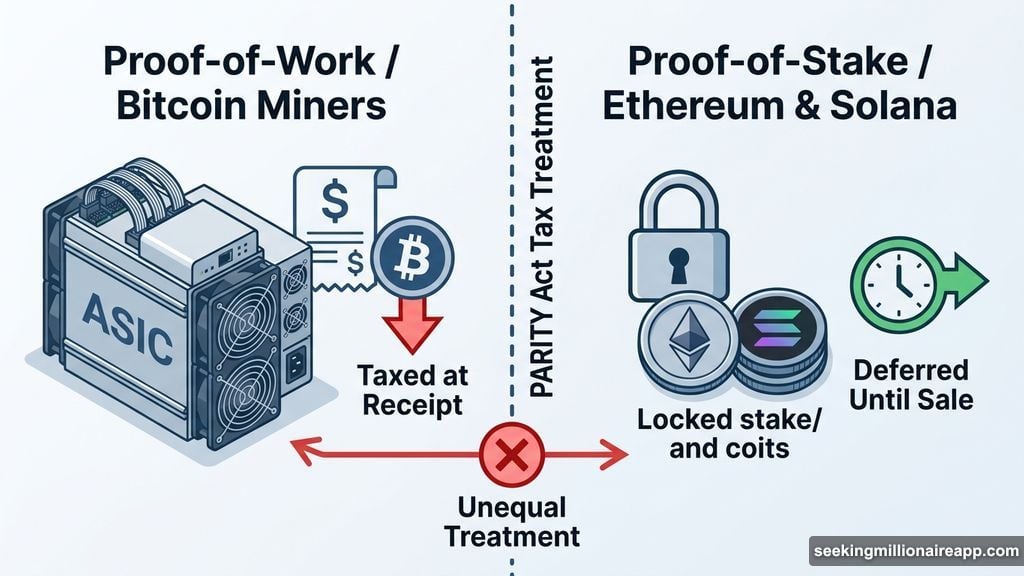

Under the current draft, earnings from cryptocurrency production would count as gross income. The fair market value at the time of receipt determines how much you owe. So far, so straightforward.

Here’s where it splits. Participants in proof-of-stake networks like Ethereum and Solana could defer those taxes until they actually sell the asset. Bitcoin miners, however, get no such relief.

That gap is exactly what’s causing the uproar.

Proof-of-Work vs. Proof-of-Stake Tax Treatment

To understand why Bitcoin advocates are angry, you need to understand the difference between these two systems.

Proof-of-stake validators lock up existing crypto to earn rewards. Their upfront costs are relatively low. Proof-of-work miners, on the other hand, buy expensive specialized hardware and pay enormous ongoing electricity bills just to operate.

So miners carry far heavier financial burdens before earning a single coin. Yet under this draft, they’d still owe taxes on rewards the moment they receive them, not when they sell.

Industry insiders call this the “phantom income problem.” You’re taxed on something you can’t easily spend, while your bills keep piling up in dollars.

Bitcoin Policy Institute Calls Out the Double Standard

Conner Brown, managing director of the Bitcoin Policy Institute, didn’t mince words. He said the draft creates a two-tier tax regime that both parties had previously agreed needed fixing.

“[The bill] offers deferral to stakers while leaving miners stuck with the same phantom income problem,” the Institute stated publicly.

Brown argued the legislation arbitrarily picks economic winners and losers. That’s a serious charge in a space where regulatory clarity has been the industry’s top demand for years.

Plus, the problem doesn’t stop at mining rewards.

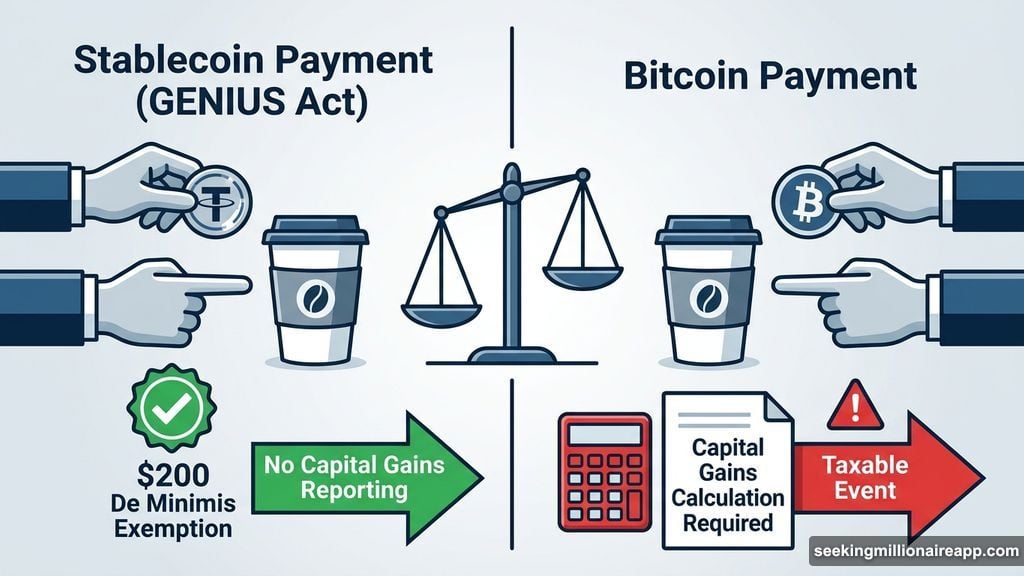

The Coffee Cup Problem: Stablecoin Payments vs. Bitcoin Spending

The draft also eases tax rules for everyday payments made with stablecoins defined under the GENIUS Act. Those transactions would get a $200 de minimis exemption, meaning small purchases wouldn’t trigger capital gains reporting.

Bitcoin doesn’t get the same treatment. Not even close.

Under this draft, buying a cup of coffee with Bitcoin could still require a capital gains calculation. That’s the kind of friction that makes Bitcoin genuinely impractical for daily retail use.

The Bitcoin Policy Institute put it bluntly: Bitcoin represents 60% of the total market cap of all digital assets, yet the bill excludes it from even basic transaction relief.

“A de minimis exemption for everyday Bitcoin transactions is necessary for the digital asset’s maturation as it grows into a global medium of exchange,” the Institute argued. “Any legislation serious about promoting parity must include it.”

It’s hard to argue with the logic. A bill called the PARITY Act that treats the largest digital asset differently from smaller stablecoins has a real branding problem at minimum, and a policy problem at its core.

Broader Industry Groups Push for Major Revisions

Not everyone is calling for the bill to be scrapped. Some groups see the draft as a starting point worth building on.

Cody Carbone, CEO of The Digital Chamber, expressed genuine excitement that a bipartisan digital asset tax discussion draft exists at all. His organization has been pushing for tax clarity throughout this entire congressional session.

But Carbone was clear that the current version needs significant work before it’s ready for anyone to celebrate.

His organization outlined several specific changes they’re demanding. Staking and mining rewards should both be taxed only when sold or disposed of, not at receipt. The de minimis exemption should extend well beyond stablecoins. Moving crypto between your own personal wallets shouldn’t count as a taxable event.

Carbone also called for simplified tax forms to eliminate duplicate reporting, and clearer rules around lending and donating digital assets. Those are practical, reasonable asks that most people in the crypto space would probably support regardless of which blockchain they prefer.

Why This Matters Beyond Crypto Twitter

If you don’t mine Bitcoin or hold crypto, you might wonder why any of this affects you. But the stakes here are bigger than tax nerds arguing over code language.

The PARITY Act shapes whether Bitcoin becomes a usable everyday currency or stays a speculative asset that’s too complex to spend. It also determines whether Bitcoin mining as an industry stays in the United States or moves to jurisdictions with friendlier tax treatment.

Carbone specifically flagged the risk of companies moving overseas if the legislation passes in its current form. That’s not just bad for crypto. It’s bad for American jobs, tax revenue, and technological leadership.

The draft still has a long road ahead. Lobbying groups on multiple sides are already pressing lawmakers hard. Whether those efforts produce meaningful changes or get steamrolled by political compromises remains to be seen.

What’s clear right now is that the Bitcoin community isn’t going to let this one slide quietly into law.