Circle just posted numbers that made investors cheer. But buried beneath the headline beats is a risk that could reshape the company’s entire earnings model.

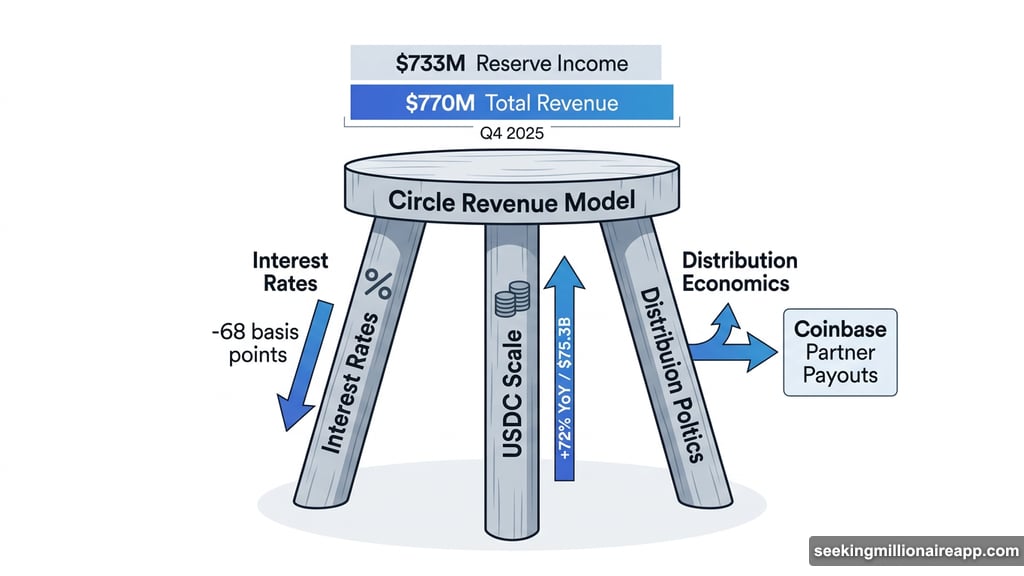

In Q4 2025, Circle reported total revenue and reserve income of $770 million. USDC in circulation hit $75.3 billion at year-end, up 72% year over year. Strong results. Clean beat. Stock reacted accordingly.

But here’s what the press release doesn’t spotlight: the most important question facing Circle right now isn’t about revenue growth. It’s about whether regulators will blow up the commercial arrangement that funds a huge chunk of that revenue.

Three Levers Power Circle’s Business

To understand the risk, you first need to understand how Circle actually makes money.

The model breaks down into three components: interest rates, USDC scale, and distribution economics. Think of it like a three-legged stool. Remove any leg and the whole thing wobbles.

Interest rates determine what Circle earns on its reserves. Right now, reserve income hit $733 million in Q4, representing a reserve return rate of 3.8%. That’s down 68 basis points year over year, meaning the interest rate environment isn’t getting friendlier.

USDC scale is the size of the reserve base itself. More USDC in circulation means more dollars sitting in reserves generating that interest. As scale grows, it can more than compensate for falling rates. That’s exactly what happened in Q4.

Distribution economics, the third leg, determine how much of that reserve income flows back out to partners who help promote and distribute USDC. This is where things get complicated.

USDC Broke Free From Crypto Price Cycles

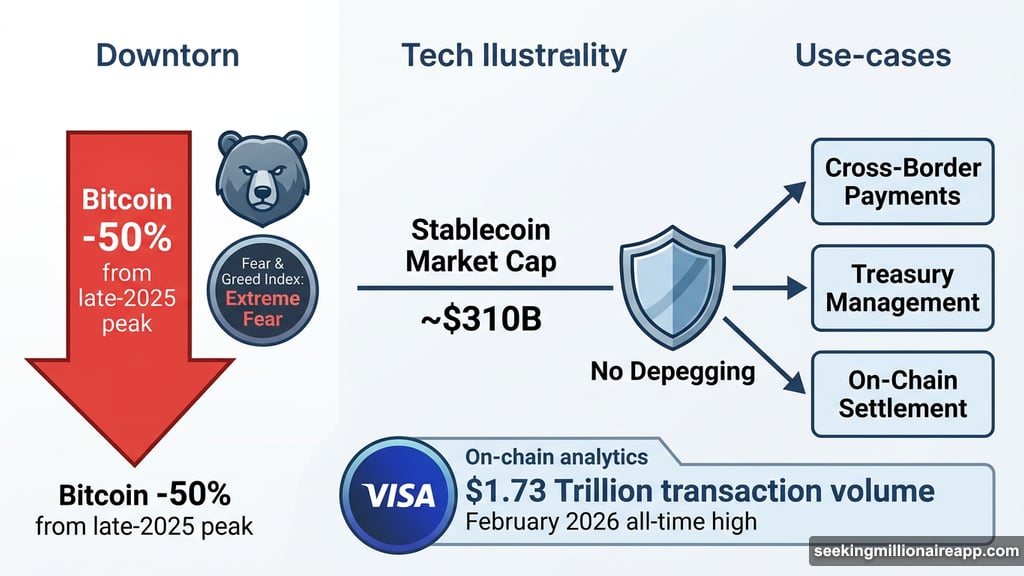

Before we get to the scary part, here’s the genuinely good news: USDC scale proved remarkably tough in a brutal market.

Bitcoin dropped nearly 50% from its late-2025 peak. By historical standards, that kind of drawdown usually triggers stablecoin redemptions, depegging incidents, and capital fleeing the ecosystem. None of that happened this time.

Total stablecoin market cap sat around $310 billion as of early 2026, still near historic highs. More striking, data from Visa’s on-chain analytics showed total stablecoin transaction volume hit a fresh all-time high in February 2026, recording $1.73 trillion in a single month. During a period when the Fear and Greed Index was printing extreme fear.

So why didn’t stablecoins collapse alongside crypto prices? A few structural shifts explain it. Stablecoins now serve real financial functions beyond crypto trading. Cross-border payments, treasury management, on-chain settlement, and business transactions all run on stablecoin rails today. That utility base provides a floor that pure speculation never could.

Plus, the infrastructure has matured. Reserve transparency is better. Regulatory oversight is tighter. Traditional finance rails are more integrated. Panic-driven redemptions are simply less likely now.

For Circle, this matters enormously. A stable stablecoin supply means a stable reserve base. A stable reserve base means more predictable reserve income. So Circle’s earnings have effectively decoupled from crypto price volatility, even if Circle’s stock price hasn’t caught up to that reality yet.

That last point is worth dwelling on. The stock still trades like a high-beta crypto proxy, swinging with Bitcoin sentiment rather than reflecting Circle’s increasingly bond-like reserve income stream. As stablecoin adoption deepens further, that mismatch between fundamentals and market perception could eventually correct, potentially driving a meaningful re-rating.

![Circle USDC circulation growth chart showing 72% year-over-year increase alongside stablecoin market stability during 2025-2026 crypto downturn]

The Coinbase Arrangement Is Under Regulatory Fire

Now for the part that keeps analysts up at night.

Circle’s distribution costs hit $461 million in Q4, up 52% year over year. A significant chunk of that flows to Coinbase under a long-standing commercial partnership. Coinbase promotes USDC, offers rewards to users who hold it, and benefits from access to Circle’s reserve income sharing. In return, Circle gets distribution reach across Coinbase’s massive retail and institutional customer base. It’s a mutually beneficial arrangement that has powered USDC’s growth.

The U.S. Office of the Comptroller of the Currency recently complicated that picture considerably.

The OCC signaled a restrictive interpretation of the GENIUS Act’s prohibition on interest payments tied to stablecoins. On the surface, the GENIUS Act prohibits stablecoin issuers from paying interest. Most of the industry assumed that meant issuers couldn’t directly pay yield to holders. Simple enough.

But the new OCC framework goes further. It suggests that “close financial ties” between issuers and crypto platforms handling their tokens would make it “highly likely” that yield is being passed to holders indirectly. In other words, if Circle shares reserve income with Coinbase, and Coinbase then offers rewards tied to USDC balances, regulators may view that entire chain as a prohibited yield pass-through.

The implications are significant. Under this reading, the Circle-Coinbase distribution structure doesn’t just bend the rules. It might fall squarely within what regulators want to prevent.

What Happens If the Distribution Model Breaks

Circle is clearly aware of this risk and has been building alternatives. “Other revenue” from non-reserve sources reached $110 million in 2025, above guidance. Products in this category include the Circle Payment Network, a near-instant stablecoin transfer system now licensed in 55 jurisdictions. Then there’s Arc Blockchain, an enterprise Layer-1 chain for programmable money. Developer tools like the Cross-Chain Transfer Protocol round out the picture.

Management has framed this as a deliberate pivot toward payment infrastructure and application-layer revenue. The narrative is compelling: reduce dependence on reserve yield, build recurring software-style revenue, become a payments company rather than a yield vehicle.

That’s the right long-term direction. But the transition takes time. And right now, exchange distribution, particularly through Coinbase, remains the dominant channel for USDC circulation growth.

![Diagram showing Circle’s three-part revenue model: reserve income rate, USDC circulation scale, and distribution partner economics with Coinbase highlighted]

How Much Risk Is Actually Priced In

The OCC hasn’t finalized its rule. Legislative negotiations around the GENIUS Act continue. Nothing is certain yet. But the uncertainty itself has real value implications.

Consider what a constrained distribution arrangement actually means. If regulators decide that reserve income sharing with Coinbase constitutes prohibited yield pass-through, Circle faces two unappealing options. Either restructure the Coinbase commercial arrangement to remove the regulatory concern, which likely means paying Coinbase differently and eating higher costs, or lose Coinbase’s promotional incentive to push USDC aggressively.

Neither outcome is catastrophic. Circle survived and grew before the current arrangement was in place. But the distribution economics leg of that three-legged stool would take a meaningful hit, at least in the short to medium term.

The rate environment is cyclical. USDC scale has shown structural resilience. Those two factors provide genuine comfort. What’s harder to model is what happens to distribution costs and distribution effectiveness if the regulatory interpretation goes the wrong way.

For investors watching Circle, the Q4 beat was real and the fundamentals are genuinely improving. The stablecoin decoupling story is legitimately interesting and probably underappreciated by a market still treating Circle like a crypto trading proxy.

But the OCC’s evolving interpretation of the GENIUS Act represents the single most important variable to monitor right now. Until that regulatory picture clarifies, the Circle-Coinbase commercial arrangement hangs in a state of uncertainty that no amount of revenue growth can fully offset.

Watch for how Circle characterizes this risk in upcoming filings. The language will tell you a lot about how concerned management actually is.