A BlackRock executive stood on a conference stage in Hong Kong and did some simple math. Asia holds roughly $108 trillion in household wealth. If even 1% of that flows into crypto, that’s nearly $2 trillion in new money entering the market. That’s about 60% of the entire current crypto market cap — from one percentage point of one region’s wealth.

The number sounds extraordinary. But at Consensus Hong Kong 2026, it felt less like a prediction and more like a problem statement. Institutional capital is massive, curious, and largely sitting on the sidelines. The question everyone was trying to answer: what does it actually take to get it moving?

The $2 Trillion Thought Experiment

Nicholas Peach, head of APAC iShares at BlackRock, made the math look easy. And honestly, it is easy math. What’s harder is the infrastructure behind it.

BlackRock’s IBIT — the US-listed spot Bitcoin ETF launched in January 2024 — has already grown to roughly $53 billion in assets. That makes it the fastest-growing ETF in history. Asian investors account for a significant share of those flows, which tells you appetite exists. But appetite isn’t the same as commitment.

The gap between interest and actual deployment is where the real story lives. And it’s a gap built from trust problems, reporting formats, regulatory uncertainty, and a fundamental cultural mismatch between how crypto works and how traditional finance operates.

Asia Is Building the On-Ramps First

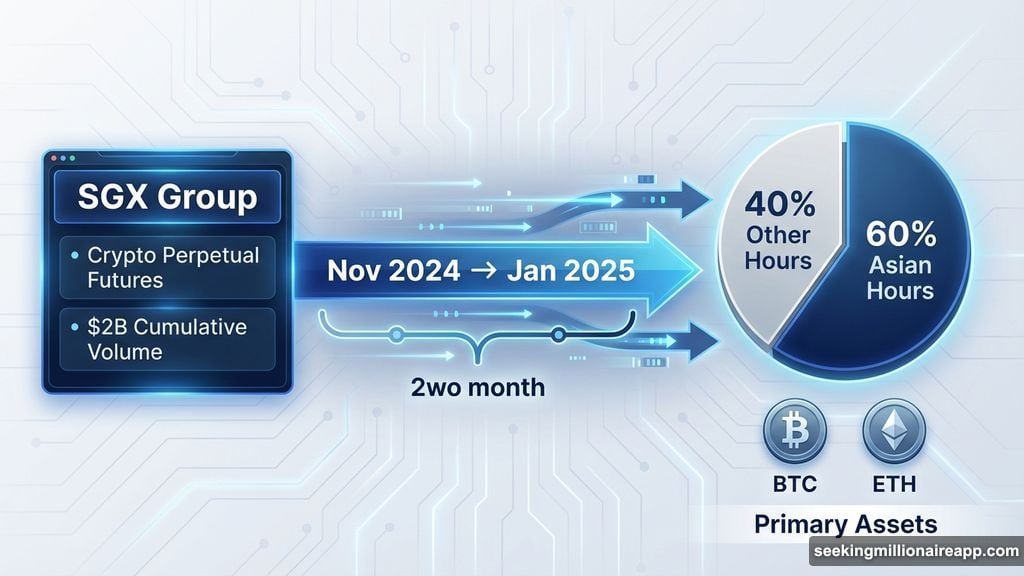

If institutions need familiar structures to invest, someone has to build those structures. Asia isn’t waiting around.

SGX Group launched crypto perpetual futures in late November and hit $2 billion in cumulative trading volume within two months. Laurent Poirot, head of product strategy and development for derivatives at SGX, called it one of the fastest product launches in the exchange’s history. More than 60% of that trading activity happened during Asian hours — a meaningful contrast to other platforms where US hours dominate.

SGX is deliberately staying focused. Institutional demand concentrates heavily on Bitcoin and Ethereum. So instead of expanding into altcoins, SGX is building out options and dated futures to complete the funding curve. It’s a disciplined approach that mirrors how traditional derivatives markets develop. Build depth before breadth.

Meanwhile, Japanese banks are developing stablecoin solutions to create regulated rails for traditional capital. Hong Kong recently approved ETFs and perpetuals, adding another layer of liquidity infrastructure. Wendy Sun of Matrixport noted that institutional behavior in the space is shifting from opportunistic to “rule-based and scheduled” — the kind of structured approach that compliance teams actually understand.

{kind=link}

TradFi Meets On-Chain Yield — and They Speak Different Languages

Here’s where things get genuinely interesting. At a side event hosted by HashKey Cloud, the conversation moved from macro numbers to the very specific friction points that keep institutional money parked on the sidelines.

Louis Rosher of Zodia Custody — backed by Standard Chartered — described a fundamental trust problem that no amount of marketing can easily fix. Traditional financial institutions lump all crypto-native firms into one category and distrust them by default. “A bank CEO with a 40-year career won’t stake it on a single crypto-native counterparty,” Rosher said.

So Zodia’s strategy is to use established banking brands as a bridge. They’re building DeFi yield access through a Wallet Connect integration, but within a permissioned framework where each application is individually vetted before being offered to clients. It’s a slower approach. But it’s the one institutions will actually use.

Steven Tung of Quantum Solutions, Japan’s largest digital asset treasury company, pointed to something even more mundane as a critical barrier: reporting format. Institutions don’t want block explorers. They want daily statements, audit trails, and custody proofs in the exact formats their compliance teams already work with. Without that, Tung argued, the vast majority of institutional capital simply won’t show up — regardless of how good the yields look.

Samuel Chong of Lido added three specific prerequisites for institutional-grade participation: protocol security, ecosystem maturity including custodian integration and slashing insurance, and regulatory alignment with traditional finance frameworks. He also flagged privacy as a hidden barrier that doesn’t get enough attention. Institutions worry that visible on-chain positions invite front-running and targeted attacks — a legitimate concern with no easy solution yet.

US Regulation Is Moving. Just Not Quickly Enough.

Anthony Scaramucci used his fireside chat to walk through the Clarity Act, the US market structure bill currently working through the Senate. Three sticking points are slowing it down: how strict KYC and AML requirements should be for DeFi, whether exchanges can pay interest on stablecoins, and restrictions on crypto investments tied to the Trump administration and its affiliates.

Scaramucci predicted the bill would pass eventually. His reasoning was blunt: younger Democratic senators don’t want to face well-funded crypto industry political action committees in their next elections. Political math, not conviction.

But he was equally direct about what’s slowing things down. Trump’s personal crypto ventures — including meme coins — are creating legislative complications. Scaramucci called Trump objectively better for crypto than Biden or Harris while simultaneously criticizing the self-dealing as harmful to the broader industry. That tension was visible on stage when Zak Folkman, co-founder of the Trump-linked World Liberty Financial, teased a new forex platform called World Swap built around the project’s USD1 stablecoin. The lending platform has already attracted hundreds of millions in deposits. Its proximity to a sitting president remains a complication that’s hard to legislate around.

Meanwhile, Asia is building without waiting. Hong Kong, Singapore, and Japan are all establishing regulatory frameworks that institutions can actually plan around. Fakhul Miah of GoMining Institutional noted that institutional onboarding now requires passing “risk committees and operational governance structures” — infrastructure that simply didn’t exist for on-chain products until recently. That’s a sign of maturity, not bureaucracy.

The Market Between Cycles

Binance Co-CEO Richard Teng addressed the October 10th crash directly. He attributed $19 billion in liquidations to macroeconomic shocks — US tariffs and Chinese rare-earth controls — rather than any exchange-specific failures. “The US equity market alone saw $150 billion of liquidation,” he noted. “The crypto market is much smaller.”

But his broader read on the market was more telling. Retail demand, he said, is more muted compared to the previous year. Institutional and corporate deployment, however, remains strong. “The smart money is deploying.”

Vicky Wang, president of Amber Premium, put concrete numbers to that shift. Institutional crypto transactions in Asia grew 70% year over year, reaching $2.3 trillion by mid-2025. Still, capital allocation stays conservative. Institutions overwhelmingly prefer market-neutral and yield strategies over directional bets. “The institutional participation in Asia, I would say it’s real, but at the same time it’s very cautious,” Wang said.

Among fund managers on the ground, the mood was noticeably more subdued. Trading teams at institutional side events were significantly smaller than the year before. Most were running near-identical strategies. The broader consensus forming in the room: crypto is becoming a license-driven business where compliance and traditional financial credibility matter more than crypto-native experience. Some participants noted that serious projects now prefer Nasdaq or HKEX IPOs over token listings — a reversal that would have seemed unthinkable just two years ago.

Blockchain’s Real Endgame Is Finance

Solana Foundation President Lily Liu may have delivered the conference’s sharpest thesis. Blockchain’s core value, she argued, isn’t digital ownership, social networks, or gaming. It’s finance and markets.

Her “internet capital markets” framework positions blockchain as infrastructure for making every financial asset accessible to anyone online. “The end state is moving into assets that have value, can also command price, and bring more inclusivity for five and a half billion people on the internet into capital markets,” Liu said.

GSR’s CJ Fong added that most tokenized real-world assets will ultimately be classified as securities, requiring crypto firms to bridge to traditional market infrastructure. That means more competition from established players. But it also means the kind of legitimacy that institutional capital actually requires before deploying at scale.

The $2 trillion that Peach described isn’t arriving next quarter. But the plumbing is being laid — in Hong Kong, Singapore, Tokyo, and on SGX’s order books — by institutions that have decided crypto is worth building for, even if they’re not quite ready to bet everything on it. That’s not hesitation. That’s how traditional finance has always moved into new territory. Slowly, carefully, and then all at once.