The SEC published comprehensive rules for tokenized securities the same day Robinhood’s CEO pitched 24/7 stock trading on blockchain. Meanwhile, Do Kwon sits in prison for running the exact scheme regulators want to prevent.

This timing isn’t coincidental. For the first time, US securities law clearly defines what separates legitimate tokenized stocks from fraudulent synthetic schemes. Plus, one $40 billion collapse taught everyone why these rules matter.

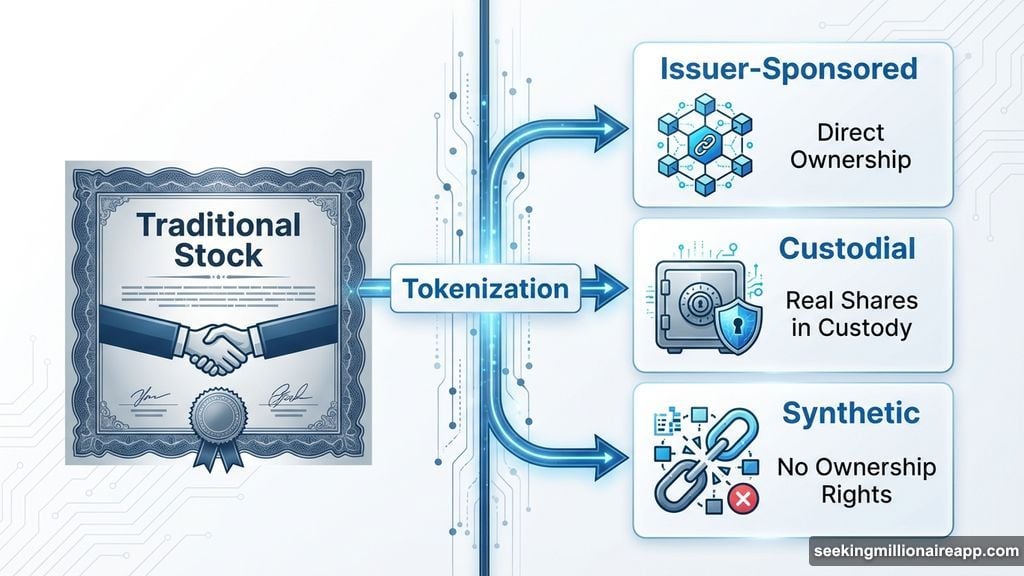

SEC Splits Tokenized Securities Into Two Models

The January 28 statement from three SEC divisions finally answers the question: what counts as a real security token?

First, there’s “issuer-sponsored tokenized securities.” Companies directly issue their own stock as tokens. The blockchain becomes the official record of ownership. When you transfer the token, you transfer actual ownership rights.

Second, “third-party-sponsored tokenized securities” exist where outside parties tokenize existing stocks. This splits into custodial and synthetic approaches.

Custodial models hold real shares in custody. Your token represents indirect ownership of those actual securities. Synthetic models give you price exposure without any ownership rights whatsoever.

That distinction matters more than most people realize. Synthetic tokens offer zero legal claim to the underlying asset. If the platform collapses, your tokens become worthless regardless of how the real stock performs.

Mirror Protocol Showed Why Rules Exist

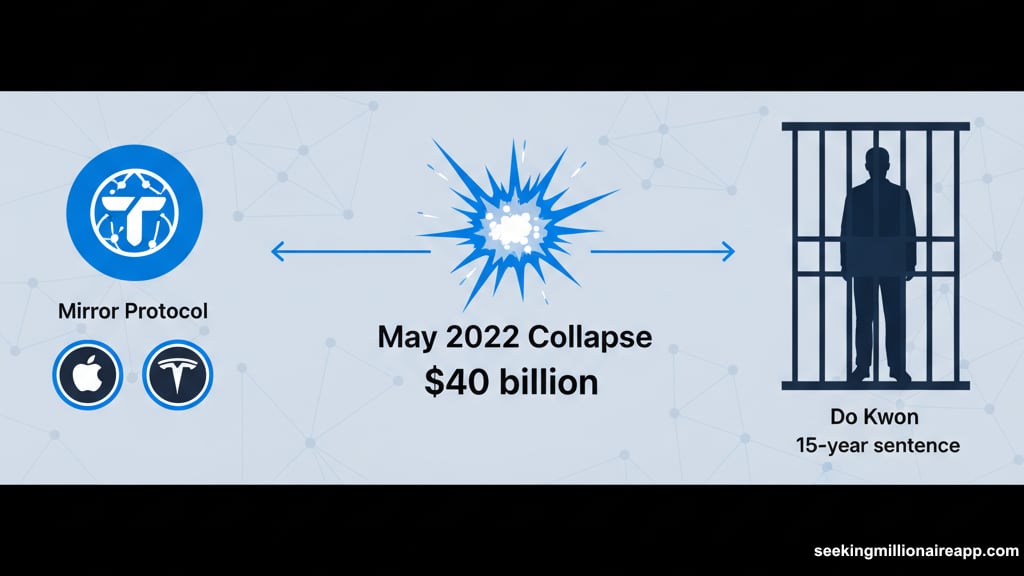

Do Kwon launched Mirror Protocol in December 2020 as the first major synthetic stock token platform. Users could trade tokens tracking Apple, Tesla, and other US stocks on Terra’s blockchain.

He marketed it as “democratizing access to global markets for disenfranchised users.” The pitch emphasized decentralization. Kwon claimed neither he nor Terraform controlled Mirror’s governance.

Complete lie. According to the US Attorney’s December 2025 sentencing statement, Kwon “secretly maintained control over Mirror and used automated trading bots to manipulate synthetic asset prices.” He also “caused Terraform to inflate key user metrics to deceive investors about Mirror’s adoption and decentralization.”

Mirror collapsed alongside UST and LUNA in May 2022. Investors lost over $40 billion total. Kwon fled, got arrested in Montenegro with a fake passport in March 2023, and received a 15-year prison sentence on December 11, 2025.

So that’s what happens when synthetic stock tokens operate without oversight or real collateral.

Robinhood Does Synthetic Tokens Right

Robinhood already offers over 2,000 US stock tokens across Europe. These are “tokenized contracts that follow stock prices” and “derivative contracts that do not grant rights to underlying securities.”

That’s the exact same category as Mirror. But the execution differs completely.

Robinhood operates as a regulated financial institution under MiFID II. The company transparently discloses that these are derivatives, not actual stock ownership. Underlying assets sit with a US-licensed institution. Investors can start with just €1 and receive dividends when eligible.

Mirror disguised itself as a “decentralized community project” to dodge regulation. Kwon secretly controlled everything. The collateral was UST, an algorithmic stablecoin that eventually collapsed to zero.

Regulation makes the difference between a legitimate product and a fraud scheme wearing decentralization as camouflage.

Tenev Wants Real-Time Settlement, Not Synthetic Tricks

Robinhood CEO Vlad Tenev published his tokenization statement January 28—exactly five years after the GameStop trading halt nearly destroyed his company.

He identified the T+2 settlement system as the root problem. Tokenization enabling real-time settlement solves it, he argues.

“T+1 is still far too long, particularly when you factor in that it really means T+3 on Fridays, or T+4 on long weekends,” Tenev wrote. Blockchain-based settlement would eliminate settlement risk entirely. Customers could trade freely 24/7 without restrictions.

Tenev announced plans to enable round-the-clock trading and DeFi access within months. Investors would self-custody stock tokens and use them for lending and staking.

This shifts Robinhood from synthetic to custodial models. It eliminates the current risk: total capital loss if the company goes insolvent. With self-custody, your tokens represent actual ownership even if Robinhood disappears.

The CLARITY Act Could Lock In Progress

Tenev praised the current SEC leadership for supporting tokenization experiments. But he urged Congress to pass the CLARITY Act, currently under consideration.

“Legislation would ensure that subsequent commissions cannot abandon or reverse the progress achieved by this SEC,” he wrote.

That’s the real concern. The SEC’s January 28 statement represents staff views without legal binding force. A future administration could reverse this stance entirely.

Do Kwon exploited exactly these regulatory gaps. He claimed “decentralization” exempted him from securities laws. The SEC’s new framework explicitly rejects that argument. But without legislation, the next SEC chair could muddy the waters again.

Synthetic Tokens Need Oversight, Not Freedom

The Mirror Protocol disaster proves one thing clearly: synthetic tokenized securities require strict regulation.

These products offer price exposure without ownership rights. That structure isn’t inherently fraudulent. But it enables fraud if operators control both the platform and collateral while claiming decentralization.

Robinhood’s European stock tokens work because the company accepts regulatory oversight. Customers understand they’re buying derivatives. Real assets back the tokens. Regulators can audit the collateral.

Kwon’s Mirror failed because he rejected oversight entirely. He manipulated prices, faked metrics, and backed tokens with his own doomed stablecoin. “Decentralization” meant zero accountability until $40 billion vanished.

The SEC framework finally draws this line explicitly. Synthetic tokens aren’t illegal. Operating them without proper disclosure, custody, and regulatory compliance is illegal.

That’s progress worth protecting. Congress should pass the CLARITY Act before someone tries to build the next Mirror Protocol.