The organization that powers most of the world’s international banking is about to put real transactions on a blockchain.

SWIFT, the messaging backbone connecting over 11,000 financial institutions across more than 200 countries, just confirmed its blockchain-based shared ledger is moving into its first MVP phase. Real-world transactions are planned for later in 2026. For an organization this deeply embedded in global finance, that’s a genuinely big deal.

Traditional Cross-Border Payments Have a Serious Problem

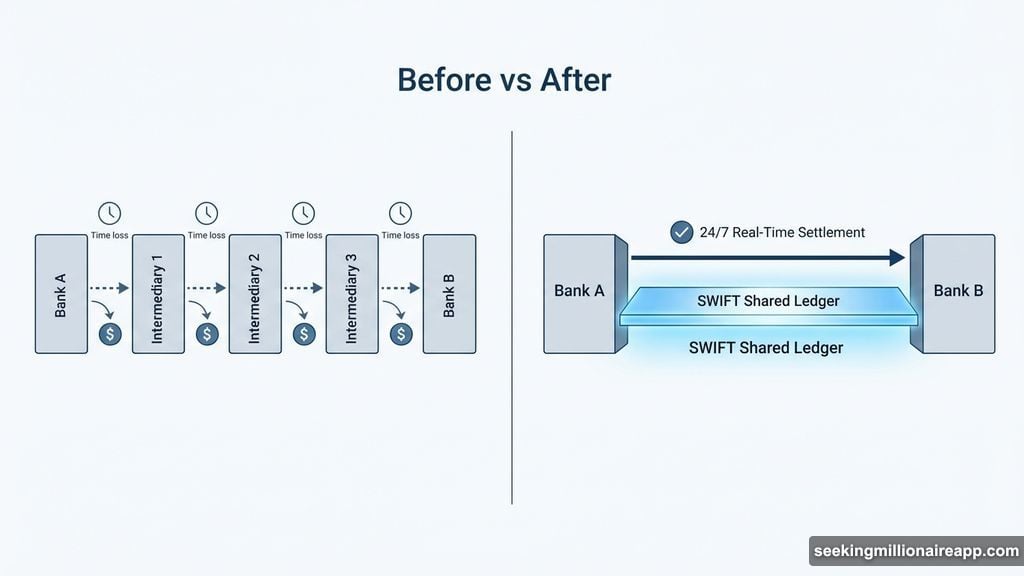

Here’s the thing about sending money internationally today. It’s surprisingly slow and clunky.

Traditional cross-border payments run through correspondent banking networks. Those networks operate within business hours, involve multiple intermediaries, and generate enormous reconciliation overhead. Think of it like passing a note through five different people before it reaches its destination. Each handoff takes time, costs money, and creates opportunities for errors.

SWIFT’s new shared ledger collapses that whole process into a single layer. Instead of separate messaging and settlement steps, everything happens together. Banks get faster payment execution, better visibility into their liquidity, and far less reconciliation work. For the institutions managing these transactions, that’s a massive operational improvement.

This Isn’t a Public Blockchain or Crypto Project

Before anyone gets the wrong idea, let’s be clear about what this actually is.

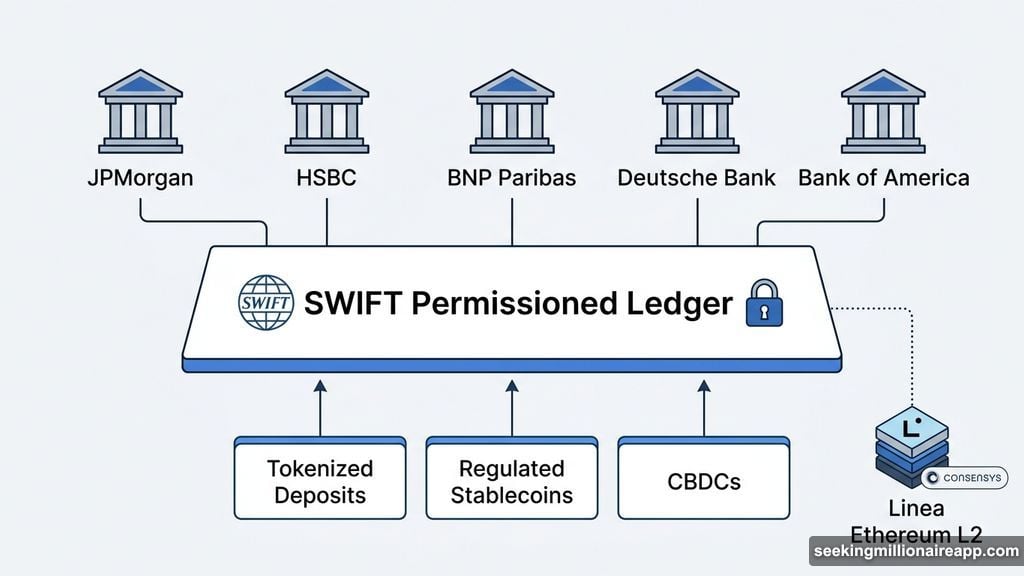

The shared ledger is not a public blockchain. It does not use a native cryptocurrency. Instead, it’s a permissioned infrastructure layer built on Linea, an Ethereum layer-2 network developed by ConsenSys. Permissioned means only approved financial institutions can participate. Nobody’s mining tokens here.

The ledger records, sequences, and validates transactions between banks using smart contracts. It supports tokenized deposits, regulated stablecoins, and central bank digital currencies (CBDCs) moving across institutions in real time, around the clock. So it borrows the technical architecture of blockchain without the speculative, open-access nature of public crypto networks.

Over 30 Major Banks Helped Build This

SWIFT didn’t design this in isolation. More than 30 global financial institutions shaped the ledger’s functionality, governance model, and future development roadmap during the design phase.

JPMorgan, HSBC, BNP Paribas, Deutsche Bank, and Bank of America were among the institutions involved. That list matters. These aren’t fringe players experimenting with crypto. They’re the biggest, most risk-averse institutions in global finance.

Their participation signals something important. When JPMorgan and Deutsche Bank spend time shaping the governance of a new settlement infrastructure, they’re not doing it out of curiosity. They’re doing it because they see real operational value.

SWIFT Isn’t Replacing Itself. It’s Adding a New Track.

One of the most interesting parts of this announcement is how SWIFT is positioning the ledger. It’s not meant to replace existing messaging infrastructure.

Instead, it runs as a parallel track. Banks can access blockchain-based settlement without redesigning their internal workflows or compliance processes. That’s a smart approach. Legacy financial systems are notoriously difficult to change. By offering the new capability alongside the existing one, SWIFT removes the biggest barrier to adoption.

What This Means for a $183 Trillion Market

Cross-border payments represent $183 trillion in annual volume. Even modest improvements to that infrastructure create enormous value at scale.

24/7 availability alone changes the game for businesses in different time zones. Right now, a payment initiated in Singapore at 6pm might not settle until the next business day in New York. With a continuously operating settlement layer, that delay disappears.

Plus, better liquidity visibility lets banks manage their capital more efficiently. Instead of holding large buffers to cover uncertain settlement timing, they can operate leaner. That frees up capital for other purposes.

The combination of speed, transparency, and reduced operational overhead makes a compelling case for adoption. And with the biggest banks already invested in its design, the network effect is already building before the first transaction clears.

The MVP goes live this year. We’ll know soon whether the real-world performance matches the promise.