Your savings account is losing the war. And most people haven’t noticed yet.

Stablecoin supply hit $300 billion in September 2025, up 75% year-over-year. That’s not speculative money chasing crypto dreams. That’s ordinary savers moving their everyday funds out of banks and into on-chain accounts that pay yield while keeping cash accessible.

The shift is quiet, structural, and accelerating fast.

The Real Problem With Your Bank Savings Account

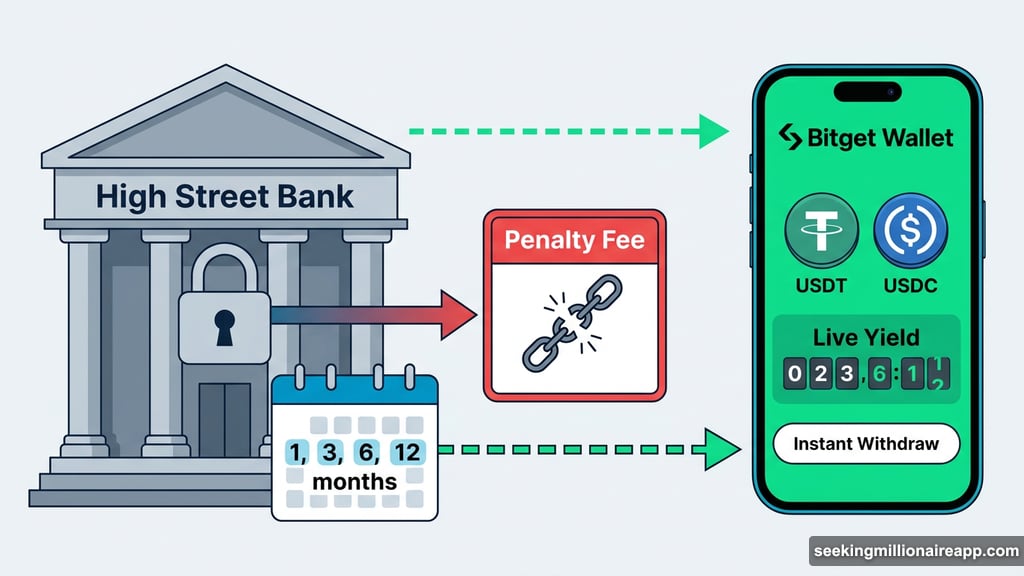

Here’s something banks don’t advertise. When you earn interest on a term deposit, you’re renting your money to the bank. They keep it for a fixed period. You get a promised return. But the moment life gets complicated, that arrangement turns painful.

Bitget Wallet CMO Jamie Elkaleh described it plainly in an interview with BeInCrypto. “If I was to go to a high street bank, I’d have to lock my money up for 1, 3, 6, or 12 months. That period is non-negotiable — or I’m paying a huge fine to pull it out. It is not like that.”

He illustrated the real cost with a story. A friend had a large sum locked in a bank deposit. When a family member fell ill and funds were needed urgently, that saver faced a brutal choice. Forfeit the earned interest, or pay a heavy penalty to access their own money.

That trade-off simply doesn’t exist in on-chain savings.

On-Chain Yield Removes the Trade-Off Entirely

Traditional banking forces a frustrating choice. You either earn interest or keep your money liquid. Pick one.

On-chain stablecoin accounts don’t force that choice. Bitget Wallet’s earn products let users stake USDT and USDC into yield-generating pools. Balances grow in real time. Withdrawals happen instantly, with no fees or penalties.

The result? Bitget Wallet recorded $200 million in quarterly earn subscriptions. That’s a 10x jump since early 2025, making it the fastest-growing segment of the wallet’s activity. For context, the wallet also processes over $900 million in monthly swap volume and nearly $5 billion in perpetuals volume. But passive stablecoin yield is outrunning everything else.

Think of it as a programmable dollar account. The wallet holds funds, generates yield, enables payments, and returns capital on demand. A traditional term deposit can’t do any of those things at the same time.

Where This Shift Hits Hardest

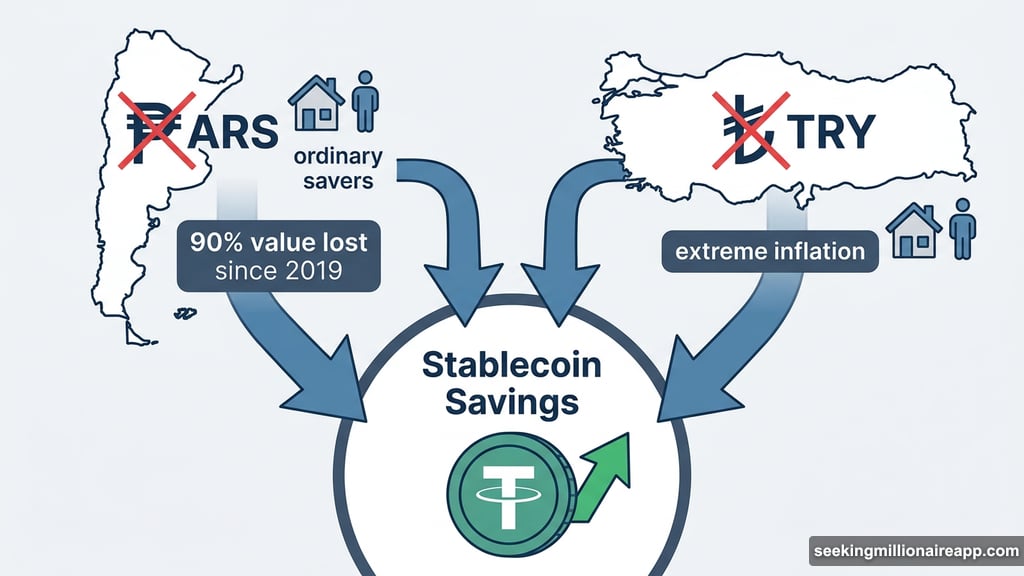

The behavioral change is most dramatic in countries where traditional finance already failed savers.

Argentina is the clearest example. The Argentine peso has lost over 90% of its value against the dollar since 2019. For ordinary households there, stablecoins haven’t become a curiosity. They’ve become the primary savings vehicle. People earn in stablecoins, save in stablecoins, and spend in stablecoins.

Turkey tells a similar story. With local currency inflation running at extreme levels, Turkish users are converting to USDT and earning yield on those holdings. Many never convert back to lira at all. The stablecoin wallet has replaced both the savings account and the bank card in a single step.

Nigeria followed a sharp path in early 2025. A sudden currency devaluation triggered a direct spike in on-chain stablecoin volume as savers rushed to preserve purchasing power.

Turkey alone processed over $63 billion in cross-border stablecoin payments in 2024, according to Morgan Stanley data. Standard Chartered identifies Egypt, Pakistan, Bangladesh, India, Brazil, and Kenya as markets facing significant deposit outflows toward stablecoins.

The motivation isn’t greed. It’s survival. These savers aren’t chasing higher returns. They want their capital to still be worth something next year.

The Numbers Behind the Migration

The macro data confirms what individual savers are already experiencing.

Standard Chartered projects the stablecoin market will reach $2 trillion by 2028. Morgan Stanley notes that stablecoin issuers now hold roughly $182 billion in US Treasury bills, placing them among the largest sovereign debt holders globally.

These aren’t speculative positions. They’re savings flows seeking three things simultaneously: stability, yield, and immediate access. Traditional term deposits offer stability and yield. They explicitly deny access. That single flaw is now driving a structural migration.

Stablecoin Yield and the Regulatory Friction

The on-chain earn model isn’t frictionless. Regulatory frameworks are catching up, and not always in savers’ favor.

The US GENIUS Act, passed in 2025, prohibits US-compliant stablecoin issuers from paying direct yields. This could reshape how American-facing wallets design their earn products. The EU’s MiCA framework creates comprehensive rules for stablecoin issuers across Europe, establishing a new compliance layer for the entire industry.

Bitget Wallet operates as a self-custodial wallet, meaning users hold their own private keys and the wallet provider never takes custody of funds. That distinction places it in a different regulatory category than bank deposits or custodial stablecoin accounts.

Jamie acknowledged that Bitget Wallet actively monitors and adapts to local regulatory requirements across all its markets. The legal landscape is still forming. But savers aren’t waiting for clarity before making decisions.

The Structural Migration Is Already Underway

The $200 million quarterly subscription figure at a single wallet is one data point in a much larger movement. Savers in developed markets are choosing flexibility. Savers in high-inflation economies are choosing survival. Both groups are arriving at the same destination: on-chain yield accounts that banks simply can’t compete with.

Traditional term deposits will still exist. Some savers will keep using them. But the structural advantage that banks held for decades, being the only place to earn interest on cash savings, is gone. On-chain alternatives offer the same stability, comparable or better yields, and the one thing banks refused to provide: your money back whenever you actually need it.

That’s not a niche product for crypto enthusiasts. That’s a better savings account for everyone.