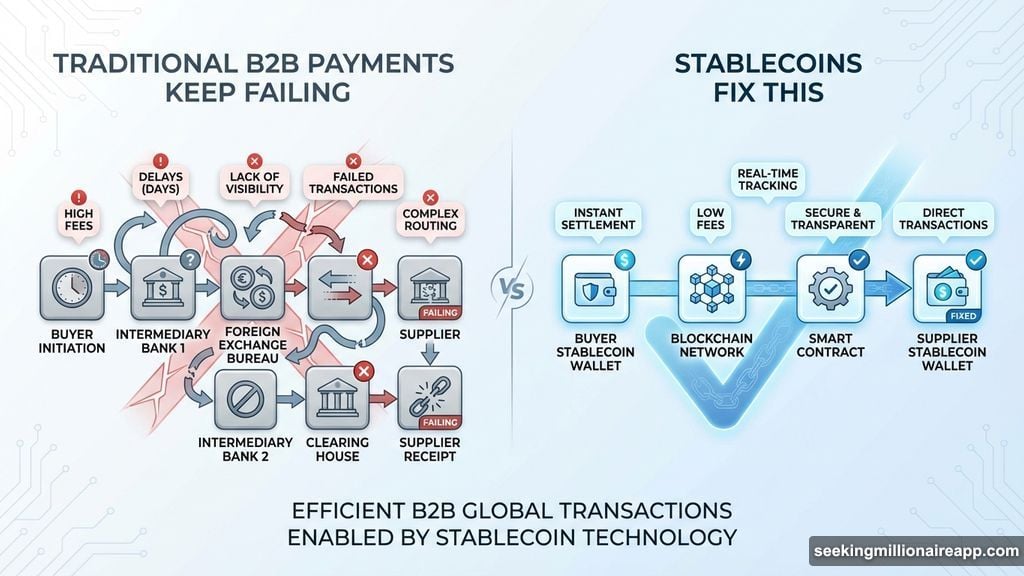

International business transfers still take days to clear in 2026. Plus, you get hit with surprise fees and manual reconciliation headaches.

The European Central Bank found that one-third of retail cross-border payments took over a day to settle in 2024. Furthermore, costs topped 3% across a quarter of global payment routes.

So, companies are desperately looking for better options. Stablecoins keep entering the conversation because they offer instant, cheap global transfers. Let’s look at what is happening behind the scenes.

Programmable Money Upgrades Treasury Logic

Most people view crypto as a speculative investment. However, stablecoins function more like reliable digital cash for business operations.

They plug directly into your internal systems through simple APIs. More importantly, these digital dollars act as programmable objects. So you can build automated rules right into your corporate money.

For example, you can set up automated sweeps to move excess balances into a central treasury wallet daily. Alternatively, you can create conditional payments that only release funds when a supplier hits specific delivery milestones.

Plus, on-chain cash segmentation lets you split funds across distinct smart contracts for payroll or taxes. Therefore, your internal accounting stays perfectly clean without manual spreadsheet updates.

DeFi Yields Create New Revenue Streams

Idle cash usually just sits in traditional banking setups. But stablecoins let you put that money to work automatically without locking it away for months.

Companies now allocate reserves into tokenized T-bills or structured on-chain lending markets. Thus, earning interest becomes a deliberate strategy rather than opportunistic trading.

Norman Wooding, CEO of SCRYPT, notes that DeFi yields respond directly to real-time supply and demand. He points out that CFOs use stablecoins to diversify returns without taking on wild crypto price swings.

Indeed, institutional platforms build risk management directly into their architecture. This gives businesses the safety they need while exploring new treasury returns.

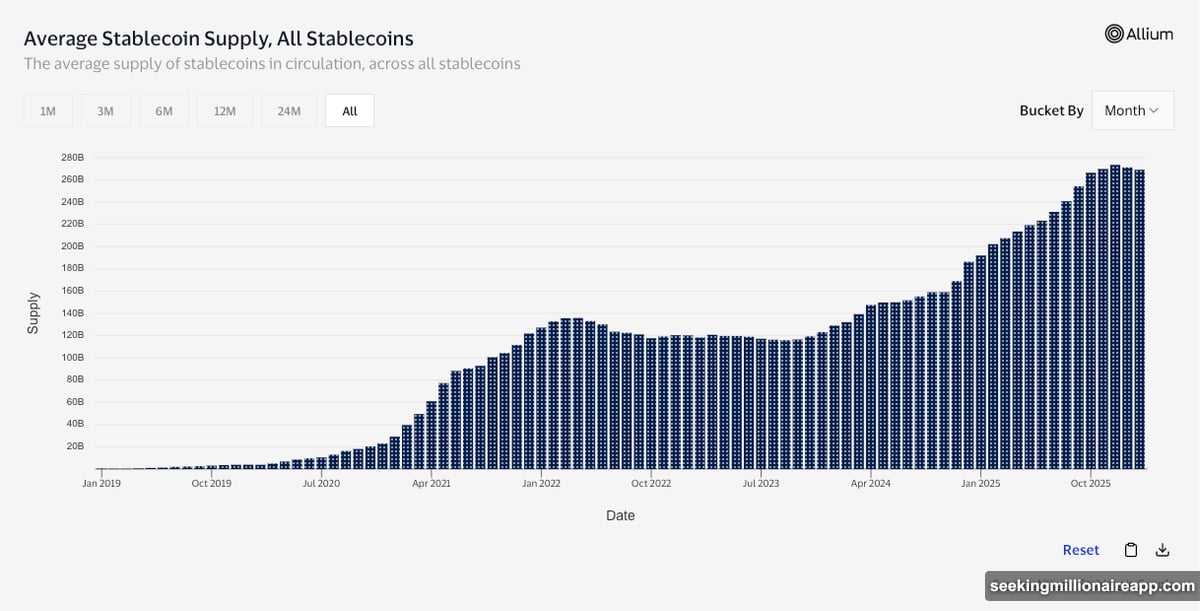

Cross-Border Settlement Volumes Beat Expectations

You might wonder if anyone actually uses these systems for real business. The numbers tell a incredibly compelling story about corporate adoption.

Total stablecoin volume hit a massive $35 trillion in 2025, according to McKinsey and Artemis Analytics. Yet much of that comes from crypto exchanges trading back and forth.

However, Visa’s recent research filtered out the speculative noise. They found $10.2 trillion in adjusted transaction volume over the last 12 months.

Specifically for B2B transactions, volumes surged from under $100 million monthly in early 2023 to over $3 billion by mid-2025. Clearly, serious companies are making the switch to digital settlement.

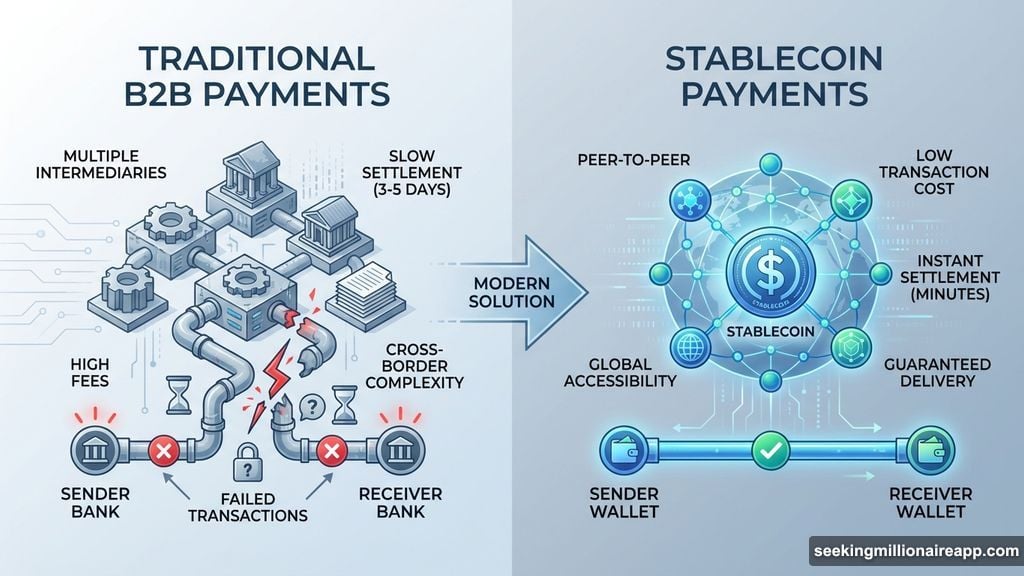

SWIFT Transfers Struggle to Keep Up

Traditional banking relies on middlemen and strict cut-off times. Consequently, delays happen constantly across different time zones.

The G20 wants 75% of wholesale cross-border payments credited within one hour by 2027. Yet many experts expect them to miss this target completely. SWIFT is trying to improve rules and cut hidden fees, but global coordination moves slowly.

Federico Variola, CEO of Phemex, explains that younger generations already prefer stablecoins over SWIFT. Traditional bank transfers remain slow and expensive. Meanwhile, stablecoins provide immediate, frictionless operations.

He adds that as reporting gets easier, structural friction disappears. So stablecoins are perfectly positioned to overtake legacy banking systems eventually.

MiCA Compliance and Liquidity Remain Hurdles

Despite the benefits, some financial leaders remain hesitant to adopt digital currencies. They worry about career risk if something goes wrong with corporate funds.

CFOs need guaranteed redemptions and reliable liquidity during market stress. Also, the Bank for International Settlements warns that stablecoins still lack the automatic trust of traditional fiat money.

Fortunately, regulators are stepping in to help build that trust. In Europe, MiCA compliance rules now enforce strict protections for digital tokens. This includes mandatory redemption at par value and rigorous stress testing.

Once these safety frameworks become standard globally, the reputational risk will vanish. Then, more corporate treasurers will feel comfortable making the leap to digital cash.

The days of waiting 48 hours for a wire transfer to clear are ending. Programmable digital money offers a clearly superior alternative for international operations.

I believe this technological shift is inevitable. The foundational highways are built, transaction volumes are rising rapidly, and regulatory clarity is finally arriving.

If your business moves money internationally, start testing these rails now. Partner with compliant institutional providers and run a small pilot program. You will quickly see why the legacy banking system’s days are numbered.