The numbers are in, and they’re not pretty. American bankruptcy filings surged sharply in the first three months of 2026, and the data tells a story that goes well beyond simple financial mismanagement.

Total US bankruptcy filings reached 150,009 cases between January and March 2026. That’s up from 132,094 during the same period last year — a 14% jump that spans both consumers and businesses alike. So what’s actually driving this, and where does it go from here?

Small Business Subchapter V Filings Hit Record Highs

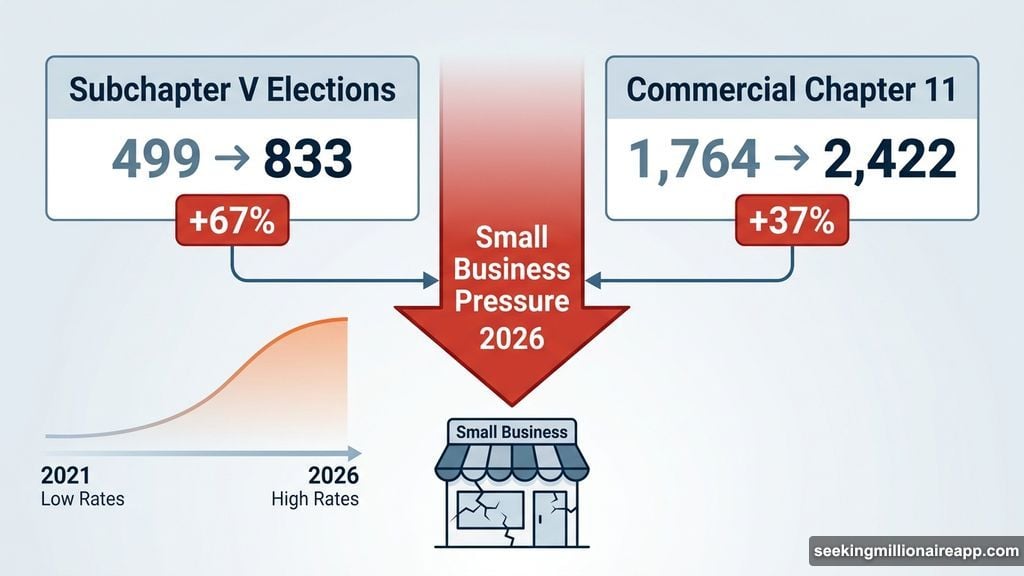

The most striking numbers come from the small business side. Subchapter V elections — a streamlined reorganization path created specifically for smaller companies — surged 67%, climbing from 499 filings to 833 in just one year.

Commercial Chapter 11 filings rose 37% as well, jumping from 1,764 to 2,422 cases. That kind of acceleration doesn’t happen by accident. It signals real structural pressure on small businesses that can’t absorb rising costs or roll over debt at manageable rates.

Plus, these aren’t just struggling startups. Many of these businesses survived the pandemic years, only to find 2025 and 2026 more financially punishing than anything that came before.

Consumer Debt Is Crushing Household Budgets

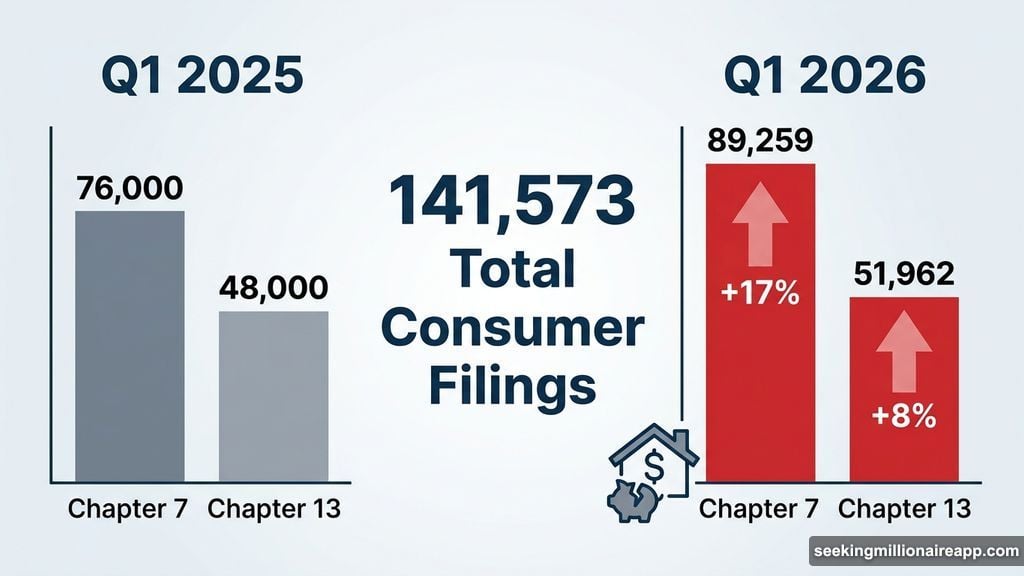

Individual filings tell the same story. Chapter 7 cases — the full liquidation path — rose 17% to 89,259. Chapter 13 filings, which allow consumers to restructure and repay debt over time, climbed 8% to 51,962. Total consumer filings hit 141,573 for the quarter.

The Federal Reserve Bank of New York’s latest household finance report provides important context here. Household debt reached $18.8 trillion by the end of Q4 2025. Credit card balances alone hit $1.28 trillion, with mortgage and student loan arrears both deteriorating noticeably.

So when Amy Quackenboss, Executive Director of the American Bankruptcy Institute, points to “persistent inflation, high interest rates, restricted credit, and global instability” as the key drivers, the data backs her up completely. These aren’t abstract economic forces. They’re the specific pressures landing on kitchen tables across the country every month.

Why High Interest Rates Keep Making This Worse

Here’s the part that should concern anyone watching this trend. Interest rates don’t just affect new borrowing. They affect every variable-rate loan, every credit card renewal, every business line of credit that comes up for refinancing.

Families and businesses that were managing debt comfortably at 2021 rates are now carrying those same balances at dramatically higher costs. That gap — between what they borrowed expecting and what they’re paying now — is exactly where bankruptcy filings come from.

The IMF projects US inflation won’t return to the Federal Reserve’s 2% target until early 2027. That means elevated borrowing costs will likely persist well into next year. And with US national debt now surpassing $39 trillion, the fiscal environment offers little cushion if conditions worsen.

Congress Is Moving — But Slowly

Lawmakers are responding, at least on paper. Senator Chuck Grassley and Representative Ben Cline recently introduced legislation that would permanently raise the small business reorganization threshold for Chapter 11 to $7.5 million. The bill would also lift the Chapter 13 debt ceiling to $2.75 million, giving more households access to restructuring protections.

Both changes would be meaningful. Higher thresholds mean more people and businesses qualify for bankruptcy protection before creditors force harsher outcomes.

But legislation moves slowly. And financial distress doesn’t wait for committee votes. The gap between when relief is introduced and when it actually reaches struggling families can span months or even years.

What These Numbers Really Signal

A 14% year-over-year spike in bankruptcy filings isn’t a blip. It’s a trend line with clear direction. And the composition of these filings matters as much as the total count.

When small business reorganizations jump 67% in a single quarter, that reflects entrepreneurs and business owners who still believe their operations are viable — if they can just get breathing room from creditors. That’s actually a healthier sign than straight liquidations. But it also means the underlying businesses need real economic relief, not just legal restructuring, to survive long-term.

The picture heading into Q2 2026 is one of compounding pressure. Inflation remains elevated. Credit remains tight. Household debt sits at record levels. And legislation that could help hasn’t passed yet.

Whether the second quarter brings acceleration or stabilization in filing numbers depends heavily on whether the Fed signals any rate relief, and whether global instability — which Quackenboss specifically cited — continues to disrupt supply chains and business confidence.

For now, the trajectory is clear. More Americans are running out of options, and the financial system they’re turning to for relief is about to get a lot busier.