The US stock market barely flinched today. Down just 0.03% at press time, the session felt more complicated than that small number suggests.

March CPI came in hot at 3.3% year over year — the highest reading since May 2024. But softer core inflation and a powerful AI-driven surge in chip stocks kept things from falling apart. So what actually happened, and what does it mean for investors watching the Fed?

Let’s break it down.

March CPI Surge: Blame the Strait of Hormuz

The Bureau of Labor Statistics reported headline CPI climbed 0.9% month over month and 3.3% year over year. That’s a big jump. And one culprit stands out clearly.

Gasoline prices exploded 21.2% in a single month. Disruptions to oil shipments through the Strait of Hormuz pushed fuel costs sharply higher, dragging the headline number up with them.

But here’s where it gets interesting. Core CPI — which strips out volatile food and energy prices — rose just 0.2% month over month and 2.6% year over year. That matched analyst expectations exactly. So Treasury yields stayed calm, and markets read the situation as a geopolitical energy shock rather than broad, persistent inflation spreading through the economy.

That distinction matters enormously for Fed rate-cut expectations. If the hot headline number reflected deep, economy-wide inflation, rate cuts would move further away. Instead, markets seem to believe this is temporary war-driven pain — not a structural inflation problem.

AI Semiconductor Stocks Pull Nasdaq Into the Green

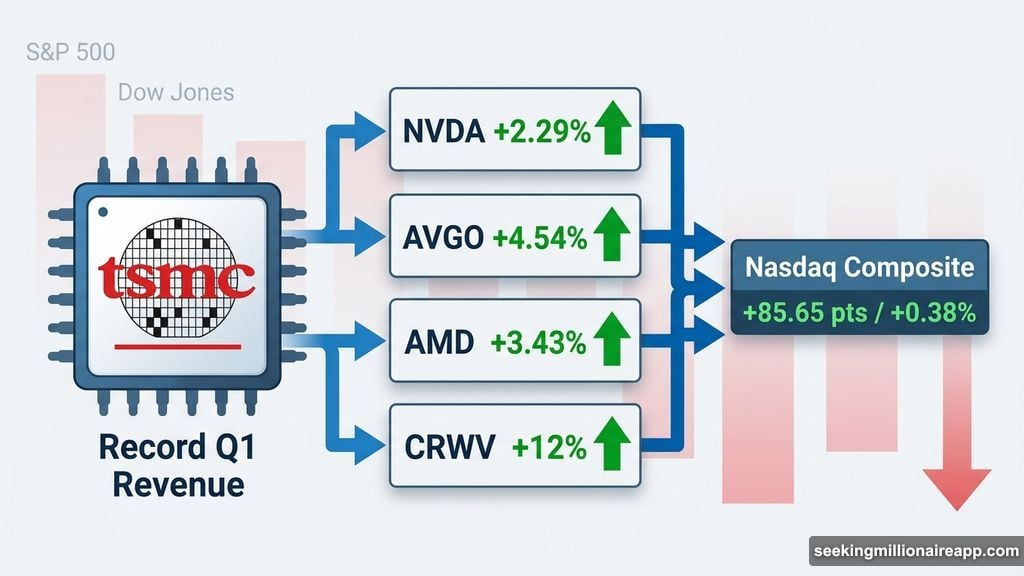

While the S&P 500 and Dow Jones both slipped, the Nasdaq Composite bucked the trend. It gained 85.65 points, or 0.38%, to close at 22,908.10. The engine behind that move? AI and semiconductor stocks, supercharged by a major earnings catalyst.

TSMC reported record first-quarter revenue, showing that demand for advanced AI chips remains strong despite geopolitical uncertainty. Investors took notice immediately.

Broadcom (AVGO) surged 4.54%. Nvidia (NVDA) added 2.29%. AMD jumped 3.43%. And CoreWeave (CRWV) leapt over 12% after the company priced an upsized $3.5 billion convertible note offering, expanded its Meta AI deal to $21 billion, and signed a multi-year agreement to power Anthropic’s Claude AI models.

That’s serious momentum in one corner of the market. But it’s also a very narrow corner.

Thin Market Breadth Signals Rotation, Not a Broad Rally

Only about 42% of stocks advanced today. That’s a telling number. When fewer than half of all issues gain ground, a rising index tells only part of the story.

Gains concentrated almost entirely in large-cap tech and materials. Meanwhile, Healthcare dropped 0.99%, with Eli Lilly falling 1.61% and AbbVie losing 1.04%. Higher inflation raises input costs for drug manufacturers, squeezing margins and making the sector less attractive on a hot CPI day.

Consumer Defensive stocks also struggled, down 0.93%. Costco fell 1.61% and Walmart dropped 1.41%. Rising fuel costs compress margins for large retailers even when they’re considered safe-haven plays.

Financial stocks slid 0.84%. JPMorgan dropped 0.45% and Goldman Sachs slipped 0.15%. Hotter headline inflation reduces the odds of near-term rate cuts, and that directly limits the net interest margin expansion banks need to grow earnings.

Where the Four Major Indexes Landed

Here’s how the session settled out across the major benchmarks:

- Nasdaq Composite: +85.65 points (+0.38%) to 22,908.10

- S&P 500: −1.78 points (−0.03%) to 6,822.88

- Dow Jones Industrial Average: −229.48 points (−0.48%) to 47,956.30

- Russell 2000: −0.96 points (−0.37%) to 261.00

The Nasdaq stood alone in positive territory. That gap between Nasdaq and the other three indexes captures exactly what today was — a tech-driven pocket of strength inside a broadly cautious session.

S&P 500 Technical Picture Looks Surprisingly Strong

Despite the mild losses, the S&P 500’s technical setup looks better than the headlines suggest. The index now trades above all four key Exponential Moving Averages (EMAs) — a situation that hasn’t happened since February. EMAs are trend indicators that weight recent price action more heavily than older data.

The 20-day EMA sits at 6,657 and is closing in on the 50-day at 6,719. The 50-day is approaching the 100-day at 6,731. Multiple bullish crossovers may be lining up.

Since touching a possible bottom of 6,318 on March 30, the S&P 500 staged a sharp V-shaped recovery, reclaiming levels last seen in mid-March. The key level to watch right now is 6,806 — the 0.618 Fibonacci retracement level. Holding above it keeps 6,939 and 7,108 as realistic upside targets. Drop below it, and the EMA cluster between 6,719 and 6,731 becomes the next support zone.

Sectors Winning and Losing on an Inflation-Heavy Day

Two sectors held up well. Basic Materials gained 0.72%, supported by strength in gold and silver as investors sought real assets to hedge against rising inflation. Utilities added 0.71%, attracting income-focused investors looking for yield on a day when inflation data dominated the conversation.

Technology gained 0.62% — but almost entirely because of the AI semiconductor cluster riding TSMC’s earnings momentum. Strip out those few big names and the sector picture looks much thinner.

One notable casualty worth watching: Palantir (PLTR) fell 1.89% after investor Michael Burry publicly criticized the company’s AI competitive positioning. That kind of headline pressure on a widely-held AI name reflects the fragility of sentiment even within the sector’s strongest pocket.

Two Big Events That Could Shift Everything

Two developments will shape the weeks ahead more than today’s CPI print.

First, weekend ceasefire talks between the US and Iran. If diplomacy makes progress, oil prices could retreat and today’s energy-driven inflation spike might look temporary in hindsight. A breakdown in talks, though, would send fuel costs climbing again — reinforcing the inflation story and making the Fed’s job much harder.

Second, the FOMC meeting on April 29. Core CPI came in soft, which keeps rate-cut hopes alive. But headline inflation surged. Whether Federal Reserve officials treat today’s numbers as a temporary war-driven energy shock or the start of a broader inflation problem will set the tone for markets through May and beyond.

The answer to that question — more than any single earnings report or technical level — will determine where stocks go from here. For now, the market seems to be giving the Fed the benefit of the doubt. But that patience won’t last forever if oil stays elevated.