Ethereum at a quarter million dollars sounds wild. But one institutional research firm just published the math to back it up.

Etherealize, a firm focused on institutional Ethereum strategy, released a new thesis arguing that ETH could realistically trade above $250,000 per coin. The logic hinges on a single big idea: what if Ethereum absorbed the monetary premium currently held by gold and Bitcoin?

That’s not a small number. And the case they’re making is surprisingly detailed.

The $31 Trillion Question

Gold and Bitcoin together hold roughly $31 trillion in combined monetary premium. That’s the value markets assign to these assets purely because people treat them as stores of value — not because they do anything productive.

Etherealize takes that $31 trillion and divides it across the 121 million ETH currently in circulation. The result? A theoretical price above $250,000 per coin.

ETH trades near $2,400 today. So reaching that target would require a roughly 105-fold increase from current levels. The firm doesn’t offer a timeline. But their argument is that the direction is inevitable, even if the pace remains uncertain.

Why ETH Beats Gold and Bitcoin on the Fundamentals

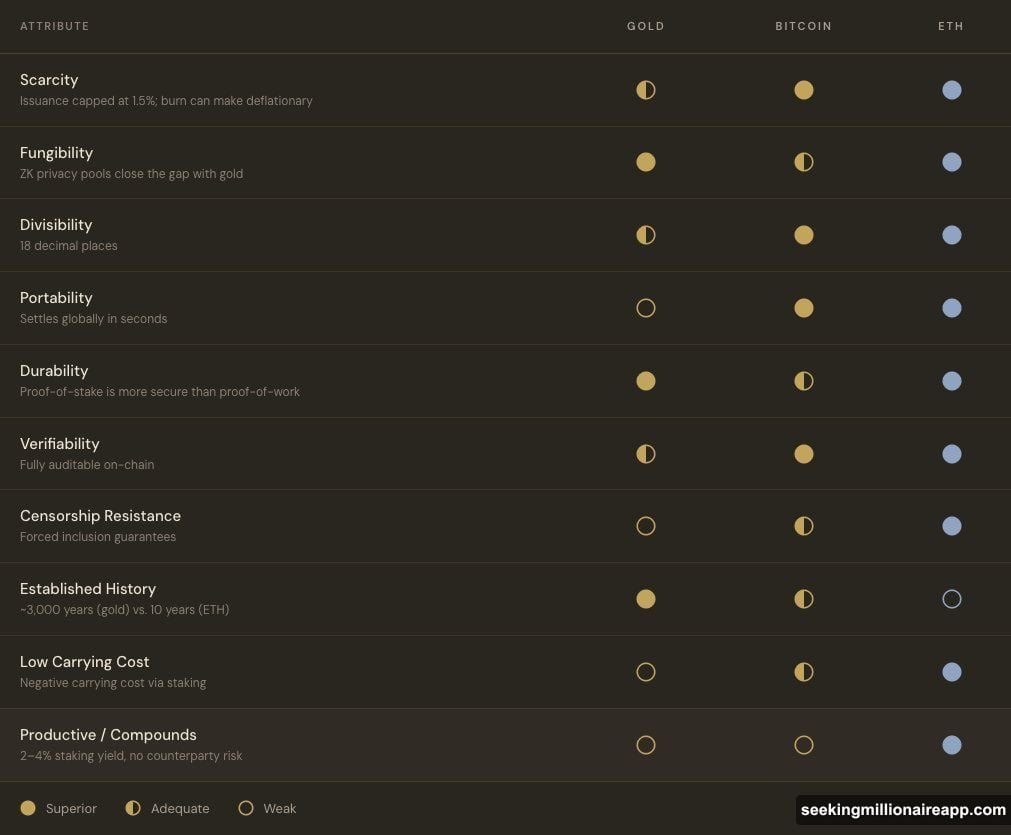

Etherealize roots its argument in Carl Menger’s 19th-century framework for what makes money good money. Menger identified scarcity, divisibility, portability, durability, and censorship resistance as the key criteria.

The firm argues ETH matches or beats both gold and Bitcoin on every single one of those measures. The only area where ETH falls short? Established history. Gold has centuries. Bitcoin has over 15 years. ETH is younger.

But history isn’t everything. And the firm points to one quality that neither gold nor Bitcoin can match.

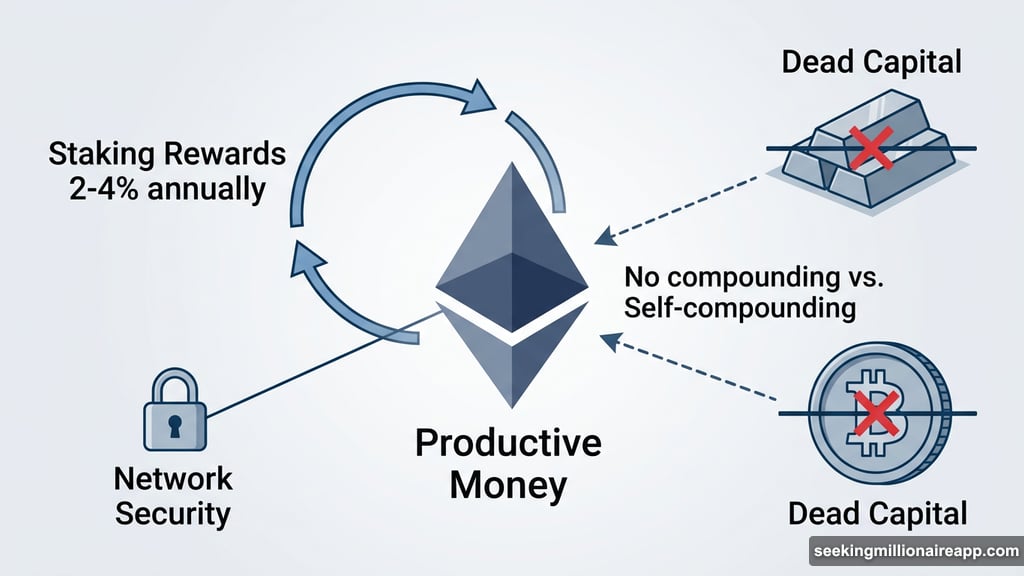

ETH Compounds. Gold and Bitcoin Don’t.

This is the heart of the thesis. Etherealize calls gold and Bitcoin “dead capital.” They sit there. They don’t grow. They don’t generate returns on their own.

ETH does something different. Staking the token currently generates between 2% and 4% annually through a combination of new issuance and transaction fees. No middleman. No counterparty risk. Just the network paying you to help secure it.

The firm even quotes Warren Buffett’s famous 2011 critique of gold: “neither of much use nor procreative.” Then they extend that same logic directly to Bitcoin. Both assets, they argue, share the same fundamental flaw — they can’t compound without someone else doing something productive with them.

“Productive money will outcompete dead capital,” the Etherealize post reads. “The only question is how long it takes the rest of the world to figure that out.”

Ethereum’s Security Model vs. Bitcoin’s

Etherealize also highlights a structural difference in how each network stays secure — and argues the gap matters more than most people realize.

Replacing all Bitcoin mining hardware worldwide would cost roughly $6.3 billion today. Ethereum, by comparison, currently has about $30 billion in staked ETH securing the network. That’s nearly five times more economic weight protecting it.

More importantly, Ethereum’s security scales with its own value. If ETH’s market cap doubles, the cost to attack the network doubles automatically. Bitcoin doesn’t work that way.

If Bitcoin’s market cap doubles, the cost to attack it stays the same until individual miners independently decide to invest in more hardware. And here’s the problem: the halving schedule makes that economic incentive weaker every four years, not stronger.

“Where Bitcoin burns energy, Ethereum deploys capital productively,” the firm writes.

One Big Caveat the Report Admits Openly

Etherealize doesn’t pretend this is a sure thing. The entire thesis depends on global markets reaching consensus that ETH functions as money — not just as a utility token or investment vehicle.

That consensus doesn’t exist yet. Most institutional investors still think of gold as the default monetary hedge and Bitcoin as digital gold. Shifting that perception across global financial markets is a massive lift.

The firm also stops well short of predicting when any of this might happen. The $250,000 figure is a target based on a specific scenario playing out fully, not a price prediction with a date attached.

Still, the argument itself is worth sitting with. ETH already has an intrinsic value floor that neither gold nor Bitcoin can claim. On-chain financial activity creates real demand for the network regardless of its monetary premium status. That’s a meaningful structural difference.

Whether the world eventually prices ETH like money or keeps treating it as something else entirely — that’s the open question that makes or breaks this entire thesis.